Council Care Cost Inheritance: Who Pays for Care Home Fees 2026? | Care Sync Experts Blog | Care Sync Experts

Council Care Cost Inheritance: Who Pays for Care Home Fees 2026?

Text to speech

00:00

5sec

Duration: 00:00

Font size

Published: 2 Mar, 2026

Share this on:

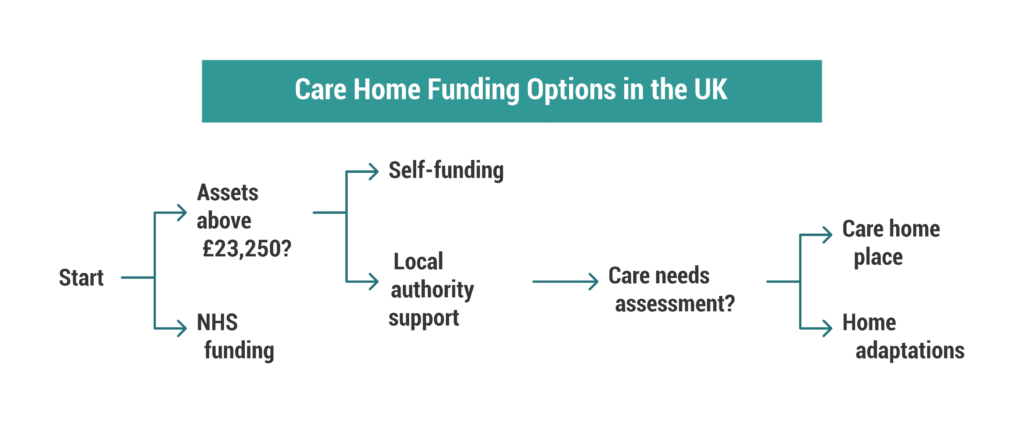

If your relative needs residential care, the council will carry out a financial assessment to decide who pays for care home fees. In England and Northern Ireland, if the person has more than £23,250 in capital (including savings and, in many cases, property), they usually fund their own care. If their assets fall below that threshold, the council contributes, or fully funds care, depending on their financial position.

When people ask about council care cost inheritance, they usually want to know one thing: will the council take the estate? The answer depends on the means test. If the person pays for care themselves, their savings or property may reduce over time. If the council funds care, it may later recover certain costs from the estate, especially where a Deferred Payment Agreement (DPA) exists.

You should also understand this clearly: there is no 7-year rule when it comes to care fees. If someone transfers money or property to avoid paying care home fees, the council can treat this as deprivation of assets. The authority may assess the person as if they still own the asset. In serious cases, it can pursue recovery from the person who received the gift.

Families often worry: are next of kin responsible for care home fees? In most situations, the answer is no. Family members do not become liable unless they have signed a contract, agreed to pay a top-up fee, or hold joint assets. The council assesses the person who needs care, not their children or wider family.

Across the UK, thresholds differ:

England and Northern Ireland: £23,250 upper capital limit

These figures shape who pays for care home fees and how much remains in the estate. Understanding this framework is the first step to navigating council care home costs confidently and protecting your family from unexpected financial shocks.

Councils calculate council care home costs through a formal financial assessment, often called a means test. They assess the person who needs care, not their children or relatives, and they look at three main areas: capital, income, and property.

1. Capital (Savings and Assets)

In England and Northern Ireland:

If capital exceeds £23,250, the person usually pays the full cost of care (self-funding).

If capital falls below £14,250, the council covers most eligible costs.

If capital sits between £14,250 and £23,250, the council contributes, but the person must pay a tariff income from savings.

Capital includes:

Bank savings

ISAs

Investments

Additional properties

In some cases, overseas assets

When people research care home charges England, they often assume the council only looks at UK savings. That is incorrect. The authority can include overseas accounts and property in its assessment.

2. Income

The council also reviews:

State Pension

Private pensions

Benefits

Rental income

The person must usually contribute most of their income toward care fees, except for a small Personal Expenses Allowance, which they keep for day-to-day needs.

3. The Family Home

Property often causes the most anxiety.

If the person lives alone and moves permanently into residential care, the council may include the property’s value in the assessment. However, the council must disregard the home if:

A spouse or civil partner still lives there

A dependent relative lives there

In certain cases, a disabled or elderly relative remains in the home

This applies whether the care involves residential placement or local authority funding for care in your own home. Home care (non-residential care) works differently: councils do not include the value of the main home in those assessments.

New Rules for Care Home Payments: What Has Changed?

Recent policy discussions around the new rules for care home payments and the proposed care home fees cap have created confusion. As of early 2026, the capital thresholds above still apply. Any future cap on lifetime care costs does not eliminate the means test or remove property from consideration.

The key point for families and caregivers is this:

The council assesses only the person receiving care. It does not automatically pursue children, and it does not combine family assets unless they are jointly owned.

Understanding how council care home costs are calculated allows caregivers to plan realistically and avoid panic decisions, especially around gifting property or transferring savings, which can trigger serious legal consequences under deprivation rules.

Do You Have to Sell the Family Home to Pay for Care?

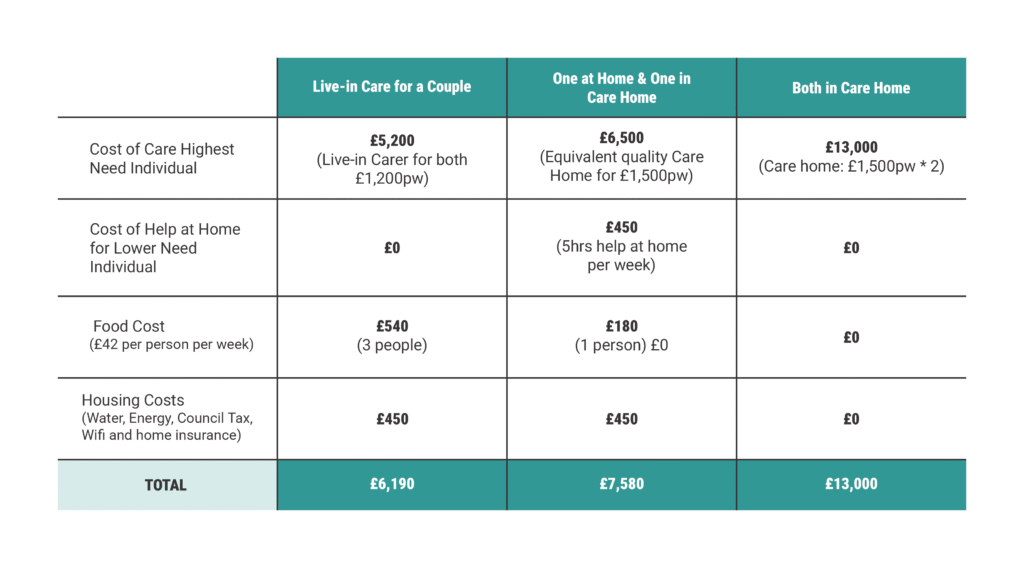

Care Costs Comparison Live-in vs. Care Homes

Many caregivers fear that the council will immediately force the sale of the family home to cover council care home costs. In reality, councils cannot require an immediate sale in most cases. They must assess eligibility first and offer lawful alternatives where appropriate.

If the person owns a home and no protected relative lives there, the council may include the property in the financial assessment once the person moves permanently into residential care. However, the law requires councils to offer a Deferred Payment Agreement (DPA) if eligibility criteria are met.

What Is a Deferred Payment Agreement?

A DPA allows the person to delay selling their home. The council pays the care home upfront and places a legal charge on the property, similar to a mortgage. When the property eventually sells, usually after death, the estate repays the council, plus interest and administrative costs.

This arrangement ensures access to council funded care homes without forcing a rushed property sale.

Key points caregivers should understand:

Interest accrues while the debt remains unpaid.

The council will obtain a property valuation before agreeing to the DPA.

The debt becomes payable from the estate, often within 90 days of death.

If the estate delays selling the property, the council can enforce repayment.

When Is the Home Disregarded?

The council must disregard the property’s value if:

A spouse or civil partner still lives in the home.

A dependent relative lives there.

A qualifying elderly or disabled relative remains resident.

In those situations, the council cannot count the home when calculating who pays for care home fees.

What About the Care Home Fees Cap?

Discussions about a national care home fees cap have created uncertainty. Even if future reforms introduce a cap on lifetime personal care costs, the means test will still apply to accommodation costs and daily living expenses. A cap does not automatically protect the full value of a property.

For caregivers, the practical takeaway is clear:

You usually do not have to sell the home immediately. But if no protected person lives there and capital exceeds the threshold, the property may eventually fund care through sale or deferred payment.

Understanding this structure helps families plan calmly instead of reacting under pressure.

Can You Give Away Property to Avoid Care Home Fees?

Many families search for ways to protect inheritance and quickly encounter advice about gifting property, moving money, or using so-called “loopholes.” Before you take any step, you need to understand how deprivation of assets works.

If someone transfers savings or property specifically to reduce their council care home costs, the local authority can treat this as deliberate deprivation of assets. The council will assess the person as if they still own the asset. In other words, gifting the house does not automatically remove it from the means test.

There Is No 7-Year Rule for Care Fees

Unlike inheritance tax, care funding does not operate under a 7-year rule. Councils can investigate transfers regardless of when they happened. If they believe the person acted to avoid care charges, they can include the gifted asset in the financial assessment.

This applies whether someone:

Transfers property to children

Moves savings into another account

Sets up certain trusts

Attempts asset hiding

Searches for ways on “how to hide savings from benefits”

The council looks at intention. If the person could reasonably foresee needing care at the time of the transfer, the authority may decide the transfer amounts to deprivation.

Can the Council Recover Money From the Recipient?

Yes. If the council determines deprivation of assets, it can:

Treat the person as still owning the asset (notional capital), or

Pursue the person who received the gift to recover unpaid care costs

This power makes so-called deprivation of assets loopholes UK highly risky. Many commercial schemes promise to protect property from care fees, but councils can challenge arrangements that exist primarily to avoid paying for care.

Is There Any Legal Way to Plan?

Legitimate estate planning does exist. Timing and purpose matter. For example, planning undertaken many years before any care needs arise, and for genuine reasons unrelated to care fees, may stand on firmer ground. However, once care becomes foreseeable, aggressive transfers can create more financial damage than protection.

Families who try to “beat the system” often trigger investigations, delay funding approvals, and increase stress during an already difficult time.

The safest approach is informed planning, not reactive transfers. Understanding how deprivation of assets works protects caregivers from costly mistakes that can unravel inheritance plans and expose recipients to repayment claims.

Caregivers often ask: are next of kin responsible for care home fees? In most cases, the answer is no.

The council assesses the person who needs care. It does not automatically pursue children, siblings, or other relatives. You do not become liable simply because you are “next of kin.”

When Might a Family Member Become Responsible?

A relative may become legally responsible only if they:

Sign a top-up fee agreement with the care home

Enter a personal contract agreeing to pay

Hold joint assets that form part of the financial assessment

If you sign a third-party top-up agreement to secure a more expensive placement, you take on a legal obligation. Fees often rise annually. Before signing, you should check whether you can afford long-term increases.

If you did not sign anything and you do not share assets, the council cannot demand that you personally pay the bill.

Can I Refuse to Pay Care Home Fees NHS?

Families sometimes ask, “Can I refuse to pay care home fees NHS?” or simply, “Can I refuse to pay care home fees?”

If the person qualifies for NHS Continuing Healthcare (CHC), the NHS covers the full cost of eligible care. In that situation, neither the individual nor the family pays. However, CHC applies only where health needs are primarily medical, not social care needs.

If the person does not qualify for CHC and exceeds the capital threshold, they must fund their own care. Refusing to pay does not stop the legal obligation. The council or care provider can pursue unpaid fees through recovery processes.

Do Dementia Sufferers Have to Pay Care Home Fees?

Families also ask: Do dementia sufferers have to pay care home fees?

A dementia diagnosis does not automatically exempt someone from paying. The council still applies the means test unless the person qualifies for NHS Continuing Healthcare. Some people with advanced dementia do meet CHC criteria, but many do not.

The key principle remains consistent:

The person receiving care pays if they exceed the capital threshold. Family members do not automatically inherit the debt unless they voluntarily agree to pay or share assets.

Understanding this distinction reduces unnecessary panic and helps caregivers make decisions based on facts rather than fear.

Who Is Responsible for Care Home Fees After Death?

When a person dies, unpaid council care home costs do not disappear. The responsibility shifts to the estate, not to family members personally.

If there are outstanding invoices, the care home or local authority will submit a claim against the estate. The executor must settle valid debts before distributing inheritance. This is where council care cost inheritance becomes practical rather than theoretical.

What Happens If There Was a Deferred Payment Agreement?

If the person used a Deferred Payment Agreement (DPA):

The council placed a legal charge on the property.

Interest accrued during the agreement.

The full balance becomes payable from the estate, usually within 90 days of death.

The property sale typically clears the debt.

If the estate delays selling the property, the council can enforce repayment.

Can the Council Recover Money From the Estate?

Yes. The council can:

Recover unpaid care costs from remaining bank funds.

Claim against the property if secured under a DPA.

In some deprivation cases, pursue recipients of gifted assets.

However, family members do not inherit personal liability. They inherit only what remains after debts are paid.

What If the Council Delayed the Financial Assessment?

Assessment delays sometimes cause individuals to pay more than necessary before council funding begins. If you believe the council acted improperly, you can:

File a formal complaint with the local authority.

Escalate to the Local Government and Social Care Ombudsman if unsatisfied.

Executors have the right to challenge incorrect billing. Councils must act reasonably and process financial assessments without undue delay.

After death, the estate pays legitimate care debts first. Only the remaining balance forms the inheritance.

Understanding who is responsible for care home fees after death helps families plan realistically and avoid unnecessary disputes during probate.

Many caregivers want to know whether they can protect part of the family home from future council care home costs. Lawful planning exists, but timing and structure matter.

Tenants in Common and Care Home Fees

Married couples and partners often own property as joint tenants. If one partner enters care and dies first, their share automatically passes to the survivor. That means the entire property may remain exposed if the surviving partner later needs care.

Some families choose to change ownership to tenants in common. This splits the property into defined shares (usually 50/50). Each person can then leave their share in a will to a trust, often called a life interest trust.

This structure can help protect half of the property for children while allowing the surviving spouse to continue living in the home.

When people search for tenants in common care home fees or tenants in common and care home fees, they are usually exploring this approach.

What This Planning Can, and Cannot, Do

It can protect the first spouse’s share after death.

It does not remove the surviving spouse’s own share from means testing.

It must form part of genuine estate planning, not a last-minute reaction to care needs.

If someone sets up ownership changes or trusts primarily to avoid care charges when care is already foreseeable, the council may investigate for deliberate deprivation of assets.

Be Careful With “Care Fee Protection” Schemes

Some commercial schemes promise guaranteed ways on how to avoid care home fees. Many rely on aggressive trust structures or asset transfers. Councils can challenge arrangements that exist mainly to reduce liability.

Proper will planning through regulated legal advice differs from last-minute asset transfers. The law allows genuine estate planning. It does not protect schemes designed solely to avoid paying assessed care costs.

For caregivers, the safest path is forward planning, not reactive transfers. Clear legal advice ensures you protect inheritance without triggering deprivation investigations or financial disputes later.

Many caregivers assume that a dementia diagnosis automatically means the NHS will pay. That is not always the case.

The council still applies the means test unless the person qualifies for NHS Continuing Healthcare (CHC). Dementia is a serious condition, but funding depends on the level and nature of the person’s needs, not the diagnosis alone.

When Does the NHS Pay?

The NHS fully funds care if the person’s primary need is health-based rather than social care. This is called Continuing Healthcare.

If approved:

The NHS covers the full cost of care.

The means test does not apply.

The person’s savings and property remain untouched for care funding purposes.

However, many dementia sufferers receive care that the council classifies as social care rather than medical care. In those cases, the standard capital thresholds apply, and the person may need to self-fund if assets exceed the limit.

Does This Change Under New Rules for Care Home Payments?

Policy discussions around new rules for care home payments and possible reforms have caused confusion. As of early 2026, the financial assessment framework remains in place. A dementia diagnosis alone does not bypass council care home costs.

What Caregivers Should Do

If your relative has advanced dementia:

Request a Continuing Healthcare assessment.

Gather medical evidence.

Challenge the decision if you believe the needs qualify.

Understanding this distinction helps families avoid incorrect assumptions about who pays for care home fees and whether inheritance will be affected.

Key Points Caregivers Must Understand in 2026

If you are navigating council care cost inheritance, keep these principles clear:

Who pays for care home fees?

The person receiving care pays if their capital exceeds the upper threshold (£23,250 in England and Northern Ireland). If assets fall below that level, the council contributes or fully funds care.

Are next of kin responsible for care home fees?

No, unless you signed a contract, agreed to a top-up fee, or hold joint assets.

There is no 7-year rule for care fees.

Councils can investigate transfers at any time. If they find deliberate deprivation of assets, they can treat the asset as still owned or recover costs from the recipient.

You do not have to sell the home immediately.

Councils must offer a Deferred Payment Agreement if eligibility criteria are met.

Dementia does not automatically mean free care.

Only NHS Continuing Healthcare removes the means test.

After death, the estate pays legitimate debts first.

Executors settle outstanding care costs before distributing inheritance.

Understanding these rules allows caregivers to plan calmly, avoid risky asset transfers, and make informed decisions instead of reacting to fear-driven myths.

Final Thought…

Care fees create stress because they mix emotion, law, and money at the same time. When you understand how council care home costs, inheritance rules, and deprivation laws actually work, you make decisions from a position of strength, not panic.

Most costly mistakes happen when families react too late. They transfer property in haste. They sign agreements without understanding liability. They assume next of kin must pay. They rely on myths about “7-year rules” or asset hiding. The law rarely rewards rushed decisions.

If you feel uncertain about eligibility thresholds, financial assessments, deprivation of assets risks, Deferred Payment Agreements, or protecting inheritance properly, do not try to navigate it alone.

Care Sync Experts supports families and care providers across the UK with clear, practical guidance on funding pathways, regulatory standards, financial assessments, and lawful planning. Whether you need clarity on who pays for care home fees, help challenging a council decision, or support understanding your rights under the Care Act framework, our team provides structured, professional advice you can rely on.

Make informed decisions. Protect your family with confidence. Contact Care Sync Experts today and move forward with clarity, not confusion.

FAQ

Can my son continue to live in my house if I go into care?

It depends on his circumstances. If your son is: – Under 18, or – Aged 60 or over, or – Disabled or otherwise dependent on you

The council must usually disregard the property when assessing care home fees.

If your son is an independent adult who does not meet those criteria, the council may include the property in the financial assessment once you move permanently into residential care. In that case, a Deferred Payment Agreement may allow him to continue living there temporarily, but the property could still form part of the eventual estate recovery.

Each situation depends on dependency, age, and vulnerability, not simply family relationship.

How much does a care home cost per week UK?

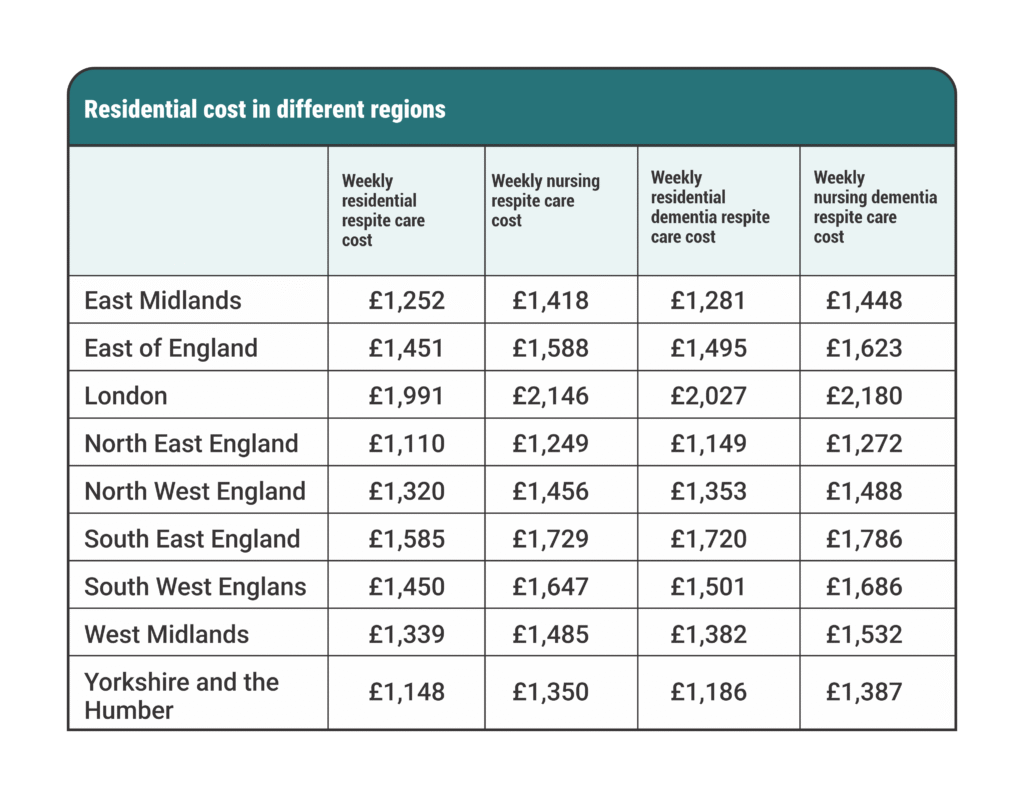

Care home fees vary by region and care needs. As of early 2026: – Residential care typically ranges between £800 and £1,200 per week. – Nursing care often ranges between £1,000 and £1,500+ per week. – Specialist dementia care can exceed these figures.

London and the South East generally sit at the higher end. If someone qualifies for NHS-funded nursing care or Continuing Healthcare, those contributions reduce or remove personal liability. Costs also rise annually, so long-term planning matters.

What assets are taken into account for care home fees?

The local authority considers: – Savings and bank accounts – ISAs and investments – Additional properties – The main home (in certain circumstances) – Pension income and benefits – Overseas assets

The council usually disregards: – Personal belongings – The main home if a protected relative lives there – Certain types of compensation payments

The authority assesses the person needing care, not wider family wealth. However, joint assets may be split 50/50 unless evidence shows otherwise.

Are children liable for deceased parents’ debts?

In most cases, children are not personally liable for a deceased parent’s debts, including unpaid care fees.

Debts are paid from the estate before inheritance is distributed. If the estate lacks sufficient funds, creditors cannot pursue children personally unless:

– The child signed a guarantee or contract, or – The debt relates to jointly held financial arrangements

Executors must settle lawful debts before distributing assets, but they do not assume personal responsibility unless they mishandle estate administration.