Where Care Excellence Meets Business Success. Transform your operations today - 0333 577 0877

Log in to CareSync Interview Preparation.

Is Carers Allowance Taxable in 2026?

Text to speech

Duration: 00:00

Font size

Published: 5 Jun, 2026

Share this on:

Yes, Carer’s Allowance is taxable in the UK. HMRC counts it as part of your taxable income, just like wages, some pensions, and certain other state benefits. However, this does not always mean you will pay tax on it. You usually only pay Income Tax if your total taxable income goes above your Personal Allowance.

Carer’s Allowance is currently £86.45 a week if you care for someone for at least 35 hours a week and meet the eligibility rules. GOV.UK lists Carer’s Allowance as a taxable state benefit, while benefits such as Personal Independence Payment, Universal Credit, Attendance Allowance, and Disability Living Allowance are tax-free.

In practical terms, tax does not usually come off your Carer’s Allowance before you receive it. Instead, HMRC may collect any tax you owe through your tax code, especially if you also work, receive a pension, or have another taxable income.

For carers, the key question is not only “is carers allowance taxable?” It is also: “What other income do I have, and does everything together take me above my tax-free allowance?”

When Would a Carer Actually Pay Tax?

A carer pays tax only when their total taxable income goes above their tax-free Personal Allowance. For 2026/27, the standard UK Personal Allowance is £12,570, which means you can usually earn up to that amount before Income Tax starts.

Carer’s Allowance counts towards that total. So if Carer’s Allowance is your only taxable income, you may not pay tax on it. But if you also earn wages, receive a private pension, get State Pension, or earn savings interest, HMRC adds those taxable amounts together.

For example, a part-time worker who also claims Carer’s Allowance may cross the tax-free allowance sooner than they expect. The same can happen to an older carer who receives pension income.

Many carers also ask, do I have to pay tax on my savings UK or do you have to pay tax on savings? Savings interest can count as taxable income too, although basic-rate taxpayers may get up to £1,000 of savings interest tax-free, while higher-rate taxpayers may get up to £500.

So the real question is not just whether Carer’s Allowance is taxable. It is whether your combined taxable income goes above your allowance.

RELATED: Early Sign of MND in 2026: What Care Businesses Should Notice First

How Much Is Carer’s Allowance in 2026?

For 2026/27, Carer’s Allowance is £86.45 per week. You may qualify if you care for someone for at least 35 hours a week and they receive a qualifying disability benefit. You do not need to live with the person or be related to them to claim.

This answers the common question, how much is Carer’s Allowance 2026? But carers should also look beyond the weekly amount. Carer’s Allowance can affect other benefits, and it can count towards your taxable income.

If you also work, check your earnings carefully. For 2026/27, Carers UK says the weekly earnings limit is £204 after certain deductions, such as Income Tax, National Insurance, and some pension contributions.

From a caregiver’s perspective, this matters because many unpaid carers try to balance work, family, and care responsibilities at the same time. A small increase in hours, overtime, or irregular pay can affect eligibility, so carers should track earnings and report changes quickly.

Is Carer’s Allowance Means-Tested?

No, Carer’s Allowance is not means-tested in the same way as Universal Credit, Pension Credit, or Housing Benefit. Your savings and your partner’s income do not usually decide whether you can claim it.

However, Carer’s Allowance still has strict rules. You must care for someone for at least 35 hours a week, the person you care for must receive a qualifying disability benefit, and your own earnings must stay within the allowed weekly limit after certain deductions.

This is where many carers get confused. The question “is Carer’s Allowance means-tested?” has a simple answer, but the earnings rule still matters. If you work and your pay goes over the limit, even by mistake, you may receive money you later have to pay back.

Carers should also check how a claim may affect other benefits. Carer’s Allowance can count as income for some means-tested benefits, and it may affect the benefits of the person you care for. Before you claim Carer’s Allowance, check the full impact, especially if the household already receives Universal Credit, Pension Credit, Housing Benefit, or income-related ESA.

READ MORE: What Is Safeguarding in Care? 2026 Update

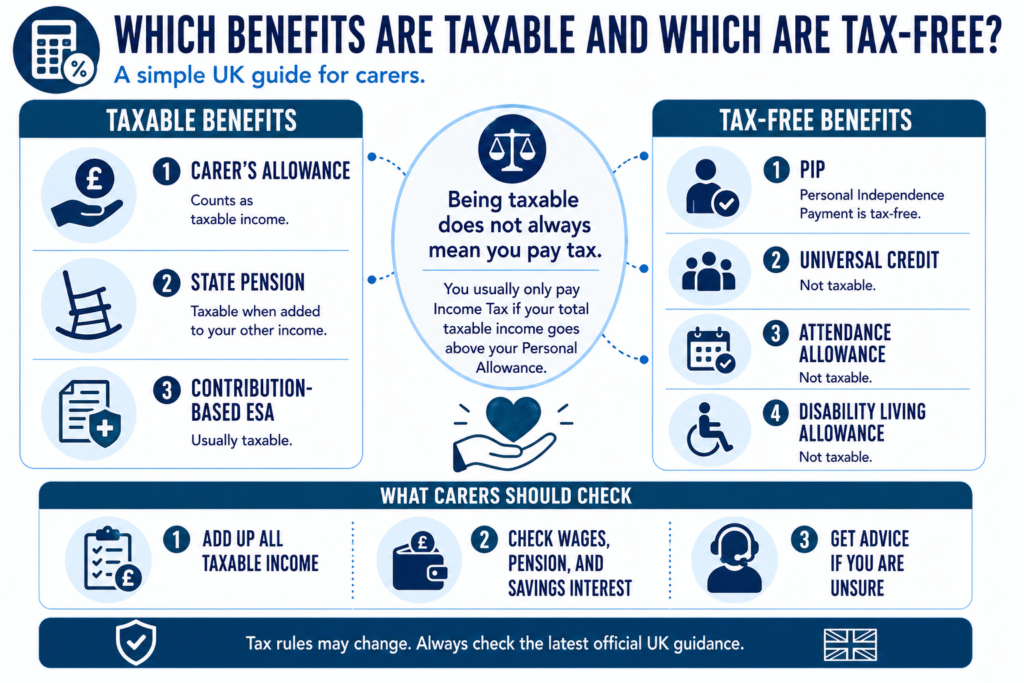

Which Benefits Are Taxable and Which Are Tax-Free?

Not every benefit counts as taxable income. This matters because many carers support someone who receives disability benefits while also managing their own Carer’s Allowance, pension, work income, or Universal Credit.

Here is the simple difference:

| Benefit | Taxable? |

| Carer’s Allowance | Yes |

| State Pension | Yes |

| Contribution-based ESA | Yes |

| PIP | No |

| Universal Credit | No |

| Attendance Allowance | No |

| Disability Living Allowance | No |

So, is PIP taxable? No. Personal Independence Payment is tax-free. Is Universal Credit taxable? No. GOV.UK lists Universal Credit as a tax-free state benefit. However, is ESA taxable? It depends. Contribution-based ESA is taxable, while income-related ESA is usually tax-free.

The State Pension works differently. Is State Pension taxable? Yes. You do not usually see tax deducted directly from the State Pension, but HMRC still counts it as taxable income. So when carers ask, “do you pay tax on State Pension?” the answer depends on whether your total taxable income goes above your Personal Allowance.

Carer’s Allowance, Pensions, and Older Carers

Many older carers ask similar questions: is State Pension taxed, do you pay tax on pension, or is the State Pension taxable? Yes, the State Pension counts as taxable income, and private or workplace pensions usually count as taxable income too.

This does not mean every pensioner pays tax. A pensioner usually pays Income Tax only when their total taxable income goes above the Personal Allowance. That total can include State Pension, private pension income, work income, Carer’s Allowance, and taxable savings interest.

So, how much can a pensioner earn before paying tax UK? In most cases, the same standard Personal Allowance applies: £12,570 for the tax year, unless personal circumstances change the allowance.

Some carers also ask, do pensioners pay Council Tax? Council Tax is separate from Income Tax. Pensioners may still pay it, but some people qualify for Council Tax Reduction, discounts, or exemptions depending on income, household circumstances, disability, or local council rules.

One helpful point: pension contributions can reduce your taxable income in the UK, depending on the type of pension arrangement and tax relief method. If you work while caring, this can matter when checking earnings and taxable income.

SEE ALSO: Carers Allowance Supplement: What Scotland’s Carers Need to Know in 2026

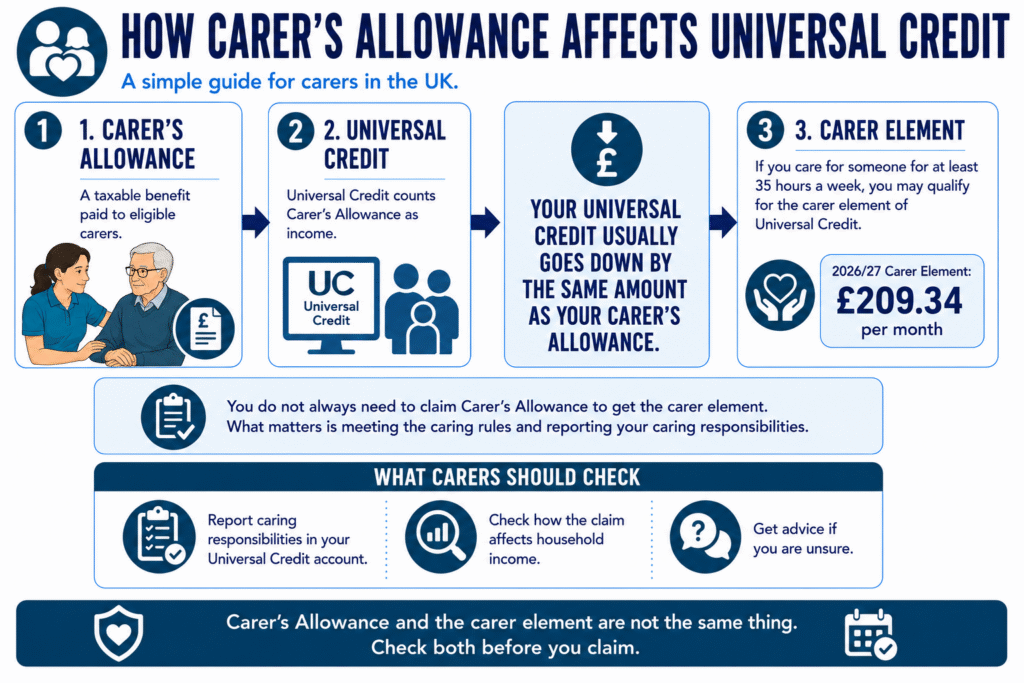

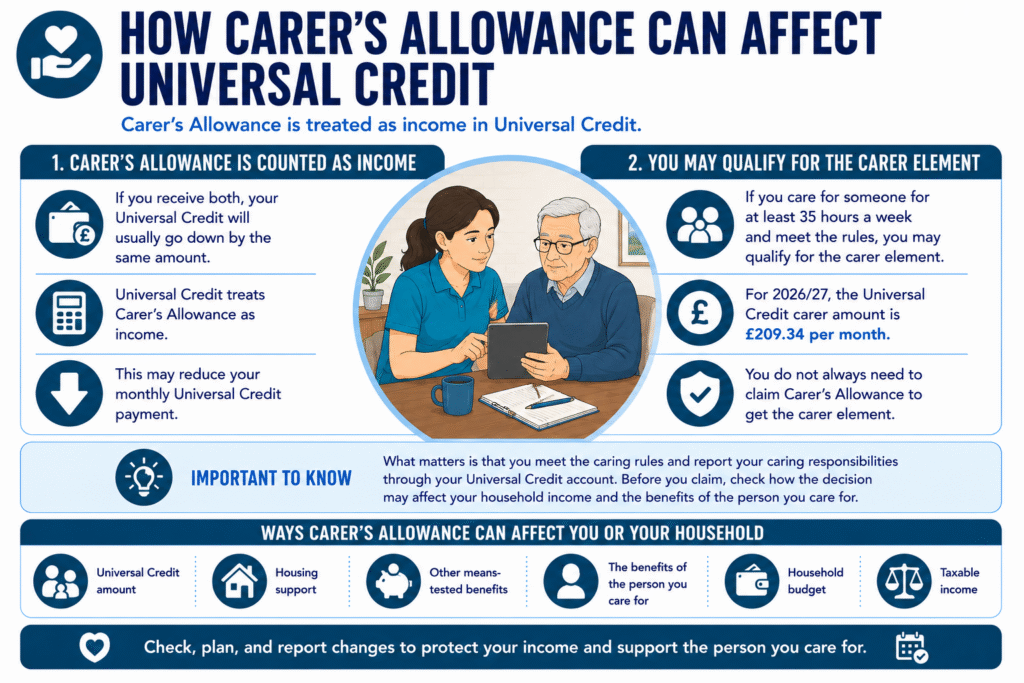

How Carer’s Allowance Can Affect Universal Credit

Carer’s Allowance can affect Universal Credit because Universal Credit treats it as income. If you receive both, your Universal Credit usually goes down by the same amount as your Carer’s Allowance.

However, this does not always mean caring leaves you worse off. If you care for someone for at least 35 hours a week and meet the rules, you may qualify for the carer element of Universal Credit. For 2026/27, the Universal Credit carer amount is £209.34 per month.

This answers the common question, how much is carers element? It is an extra amount added to your Universal Credit calculation; it is not the same thing as Carer’s Allowance.

You do not always need to claim Carer’s Allowance to get the carer element. What matters is that you meet the caring rules and report your caring responsibilities through your Universal Credit account. Before you claim, check how the decision may affect your household income and the benefits of the person you care for.

MORE: Support Hose Compression: Benefits, Side Effects, and Safe Use

How to Claim Carer’s Allowance and Who to Contact

You can claim Carer’s Allowance online through GOV.UK or by post. Before you apply, check that you care for someone for at least 35 hours a week, meet the earnings rules, and understand how the claim could affect your benefits or the benefits of the person you support.

You will usually need details such as your National Insurance number, bank details, employment information, and details of the person you care for. The person you support must also receive a qualifying disability benefit, such as PIP daily living, Attendance Allowance, or the middle or highest care rate of DLA.

If you need help, use the official Carer’s Allowance number listed on GOV.UK or contact the Carer’s Allowance Unit. Avoid relying on old phone numbers from third-party websites, as contact details can change.

A claim can sometimes be backdated, so apply as soon as you know you may qualify. Also, report changes quickly, especially if your earnings, caring hours, education status, or the cared-for person’s benefits change.

Final Advice for Carers

Carers already carry enough responsibility, so tax and benefit rules should not become another hidden pressure. If you receive Carer’s Allowance, treat it as taxable income, check your total income, and report changes before they turn into overpayments or unexpected tax bills.

The key question is not only “is carers allowance taxable?” The better question is: “How does Carer’s Allowance affect my full financial situation?” That includes wages, pensions, savings interest, Universal Credit, Pension Credit, Housing Benefit, and the benefits of the person you care for.

If you feel unsure, check GOV.UK, speak to HMRC, contact the Carer’s Allowance Unit, or get independent benefits advice. A few minutes of checking can protect your income, reduce stress, and help you keep supporting your loved one with more confidence.

At Care Sync Experts, we help carers, families, and care providers understand care-related money, benefits, and support decisions in plain English, so they can make informed choices without feeling overwhelmed.

Need Clearer Guidance on Care, Benefits, and Support?

Carer rules can feel confusing, especially when tax, benefits, and family responsibilities overlap.

At Care Sync Experts, we help carers, families, and care providers understand care-related decisions in plain English, so they can act with clarity, confidence, and less stress.

Get practical guidance that helps carers make informed decisions.

FAQ

Who cannot claim Carer’s Allowance?

You usually cannot claim Carer’s Allowance if you study for 21 hours a week or more, earn more than £204 a week after tax, National Insurance, and allowable expenses, or do not meet the basic caring rule of at least 35 hours a week.

You also cannot usually get the full amount of Carer’s Allowance and State Pension at the same time; if your State Pension is £86.45 a week or more, you will not receive a Carer’s Allowance payment.

Does Carer’s Allowance affect anything?

Yes. Carer’s Allowance can affect the benefits you receive and the benefits of the person you care for. GOV.UK also says carers may have to pay tax on it if their income goes above the Personal Allowance.

It can still help because each week you receive Carer’s Allowance, you automatically get National Insurance credits, which can protect your State Pension record.

How do I report Carer’s Allowance changes?

You can report Carer’s Allowance changes online through the Carer’s Allowance service or contact the Carer’s Allowance Unit by phone or post.

Report changes such as starting or leaving a job, earning more than £204 a week, changing address, stopping care, providing less than 35 hours of care, taking a holiday, going into hospital, or the person you care for going into hospital or a care home.

What’s the difference between a Carer Payment and a Carer Allowance?

In Australia, Carer Payment is income support for someone who provides constant care to a person who needs care for at least six months or is at the end of life. Carer Allowance is a separate set-rate payment; Services Australia says it is $162.60 each fortnight and is not part of taxable income. Depending on your circumstances, you may be able to get both.

Would you like to receive update from CareSync Experts?

All rights reserved. Copyright © - Care Sync Experts.