What Is the Retirement Age UK for Female Workers in 2026? | Care Sync Experts Blog | Care Sync Experts

What Is the Retirement Age UK for Female Workers in 2026?

Text to speech

00:00

5sec

Duration: 00:00

Font size

Published: 21 May, 2026

Share this on:

The current retirement age UK for female workers is 66, which matches the current state pension age UK for men. However, the government plans to gradually increase the State Pension age to 67 for people born on or after April 6, 1961.

Women born between April 6, 1960, and March 5, 1961, will reach State Pension age between 66 and 67 depending on their exact birth date. This transition causes confusion for many caregivers, especially those who planned to retire earlier under older pension rules.

For many care workers, the biggest question remains: is State Pension age 66 or 67? The answer depends entirely on your date of birth. While some women can still claim at 66, younger age groups will need to wait until 67 before receiving their State Pension.

Here is a quick breakdown of the current rules:

Women born before April 1950 reached State Pension age at 60

Women born between April 1950 and April 1953 reached pension age between 60 and 65

Women born between April 1953 and April 1960 now retire at 66

Women born after April 1961 will retire at 67

The government reviews pension ages regularly because people now live longer and often work later in life. However, these changes affect caregivers differently. Many carers work physically demanding roles that become harder to sustain into their late 60s.

If you are unsure about your exact retirement date, use the official UK State Pension age calculator or the UK State Pension calculator on GOV.UK to check your personal timeline accurately.

Many people discussing the state pension age UK work in office-based jobs, but caregivers often face a very different reality. Home carers, support workers, healthcare assistants, and residential care staff regularly spend long hours lifting, walking, assisting clients, and handling emotionally demanding situations.

Because of this, changes to the gov uk retirement age affect care workers more directly than many other professions.

For decades, many female caregivers expected to retire earlier. Some planned their finances around retiring at 60 or 65, only to discover that the pension timetable had changed. This shift has forced many experienced carers to continue working longer than they originally expected.

The challenge becomes even greater in domiciliary care. Many carers travel between clients, work irregular shifts, and manage physically demanding tasks daily. Reaching the new state pension age UK can feel difficult for workers already dealing with fatigue, stress, or health concerns later in life.

At the same time, the care sector continues to rely heavily on experienced female workers. Many providers now struggle with retention because older carers delay retirement while younger workers hesitate to join demanding care roles.

Understanding the current pension rules helps caregivers plan more confidently. It also helps care providers support older staff members with flexible schedules, retirement planning resources, and workplace pension guidance before they reach retirement age.

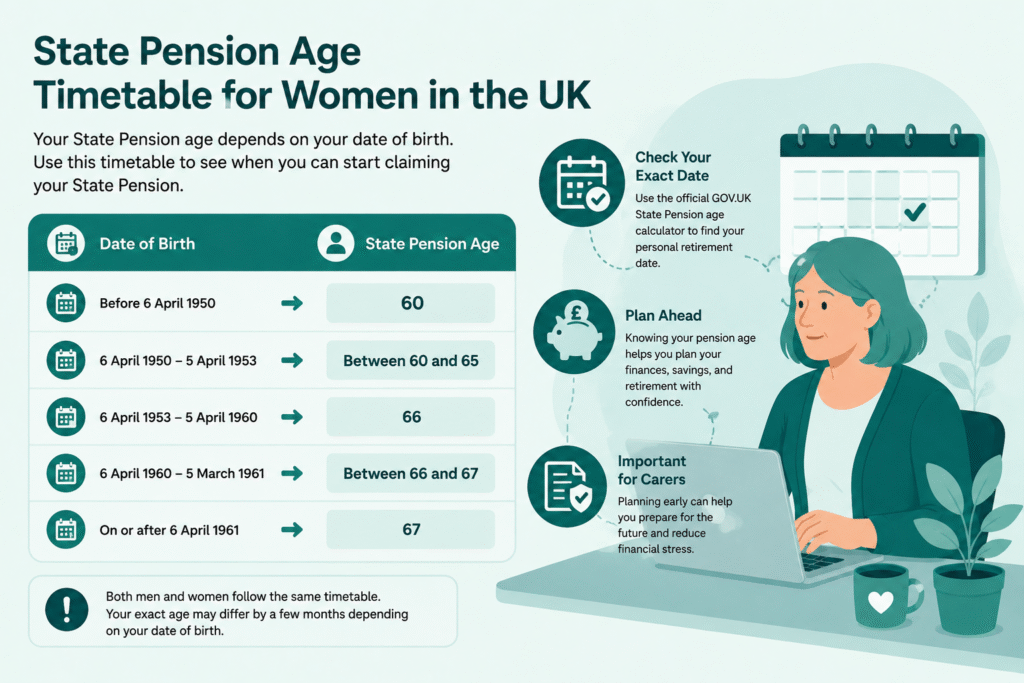

The current state pension age timetable explains when women in the UK can start claiming their State Pension. Your exact retirement age depends entirely on your date of birth.

For many caregivers, understanding this timetable helps with financial planning, workplace pension decisions, and deciding how long they may need to continue working in care roles.

Date of Birth

State Pension Age

Before April 6, 1950

60

April 6, 1950 – April 5, 1953

Between 60 and 65

April 6, 1953 – April 5, 1960

66

April 6, 1960 – March 5, 1961

Between 66 and 67

On or After April 6, 1961

67

Many people still ask, “Is State Pension age 66 or 67?” The answer depends on where your birth date falls within the government transition period.

The government increased the pension age gradually to reflect longer life expectancy and rising pension costs. Today, both men and women generally follow the same pension timetable, unlike previous decades when women could retire earlier.

Care workers should pay close attention to these dates because even a few months can affect retirement plans, savings goals, and workplace pension access. Many caregivers also combine State Pension income with private or workplace pensions to retire more comfortably.

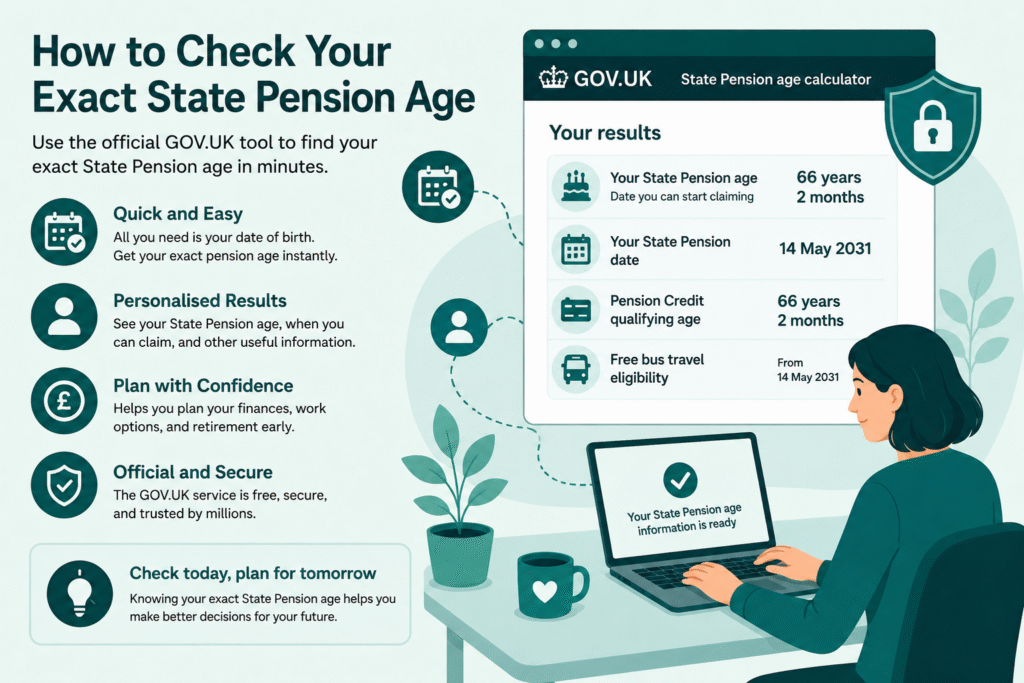

How to Check Your Exact State Pension Age

Check your state pension age now

Many caregivers feel confused about their exact retirement timeline because the UK pension changes rolled out gradually over several years. Even people born only months apart may reach retirement age at different times.

The easiest way to confirm your date is by using the official UK State Pension age calculator on GOV.UK. The tool shows:

your exact State Pension age

when you can start claiming

your Pension Credit qualifying age

eligibility for free bus travel in some areas

The official UK State Pension calculator only requires your date of birth. After entering your details, the system immediately shows your personal pension timeline.

This step matters because the current gov uk retirement age rules continue to change gradually. Checking your exact pension age early helps caregivers prepare for:

retirement savings

reduced working hours

workplace pension access

future care costs

income planning

It is also important to understand that the State Pension differs from private or workplace pensions. Many care workers can access workplace or personal pension schemes earlier, often from age 55, although this minimum age will rise to 57 from April 2028.

For caregivers working physically demanding roles, reviewing both State Pension and workplace pension options early can make retirement planning less stressful later in life.

How Much Is State Pension UK Care Workers Can Receive?

Many caregivers approaching retirement ask two important questions: how much is State Pension and will it provide enough income to stop working comfortably?

The full new State Pension in the UK currently pays over £11,000 per year, although the exact amount changes annually because the government reviews pension payments each year under the “triple lock” system.

However, not every care worker receives the full amount.

Your final pension depends mainly on:

your National Insurance contribution record

how many qualifying years you have built up

periods spent out of work

part-time employment history

This issue affects many women in care roles. Some caregivers reduce their working hours or leave employment temporarily to raise children, care for relatives, or manage health conditions. These career breaks can reduce overall pension contributions and lower future payments.

When asking how much is State Pension UK residents can receive, it is important to understand that most people need around 35 qualifying National Insurance years to receive the full new State Pension.

Many care workers also rely on:

workplace pensions

private pension schemes

personal savings

part-time work after retirement age

Because caregiving roles can become physically demanding later in life, financial planning matters even more. Checking your pension forecast early allows you to identify contribution gaps and decide whether you need additional retirement savings before reaching State Pension age.

Retirement Age UK for Male and Female Workers: Is There Still a Difference?

Planning for a secure retirement

Many people still believe women can retire earlier than men, but that is no longer the case. Today, the retirement age UK for male and female workers follows almost the same timetable.

The government introduced these changes to equalise pension ages across the UK. As a result, both men and women now generally reach the state pension age UK at 66, with a gradual increase to 67 already underway for younger age groups.

Historically, women could claim their State Pension at 60 while men waited until 65. However, the government began phasing out this gap through several pension reforms designed to reflect longer life expectancy and changes in the workforce.

For caregivers, these changes created major financial and retirement planning challenges. Many female care workers built long-term plans around retiring earlier, especially after decades spent in physically demanding care roles.

Today, when people ask, “What is the retirement age in the UK?”, the answer usually depends more on date of birth than gender.

Understanding this shift matters because many caregivers still assume older retirement rules apply to them. Checking your exact State Pension age early helps avoid unexpected delays in retirement planning and allows you to prepare more realistically for later-life income needs.

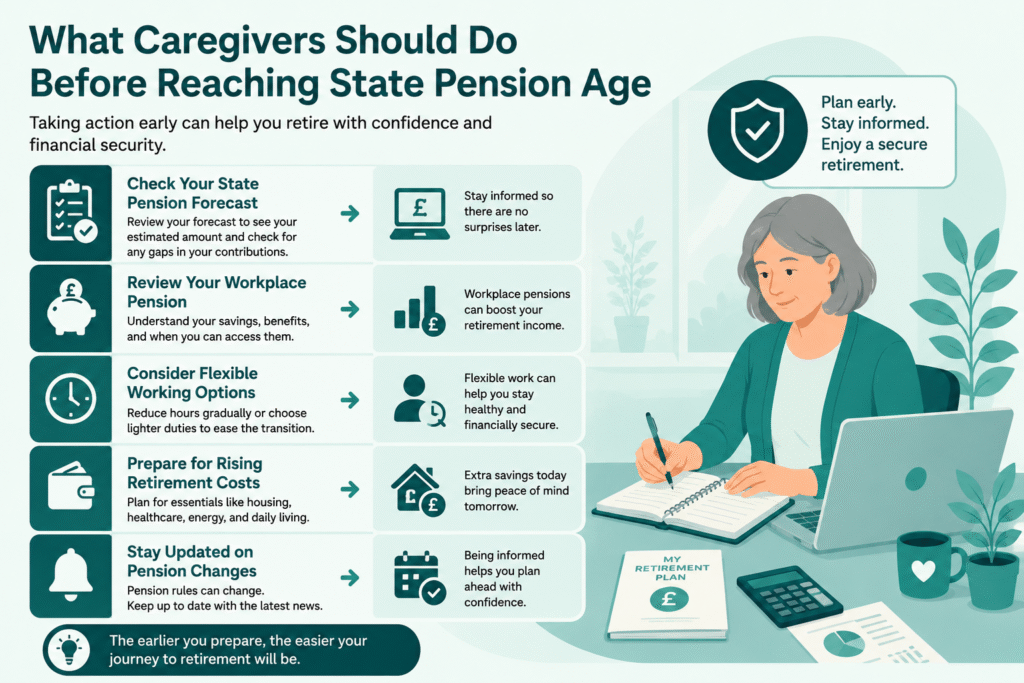

What Caregivers Should Do Before Reaching State Pension Age

Retirement Age UK for Female Workers in 2026?

Reaching the retirement age UK for female care workers now requires more planning than ever before. Many caregivers continue working longer because of rising living costs, delayed pension ages, or gaps in retirement savings.

Taking action early can make retirement less stressful and help you avoid financial surprises later.

Here are some important steps caregivers should take before reaching State Pension age:

Check Your State Pension Forecast

Review your pension forecast through the official GOV.UK service to see:

your estimated pension amount

qualifying National Insurance years

any contribution gaps

This helps you understand whether you will receive the full State Pension or a reduced amount.

Review Your Workplace Pension

Many care providers offer workplace pension schemes alongside the State Pension. Checking these savings early helps you understand your total retirement income more clearly.

Consider Flexible Working Options

Some caregivers choose to reduce hours gradually instead of stopping work completely. Flexible schedules, lighter duties, or part-time care roles can help older workers manage the physical demands of caregiving more comfortably.

Prepare for Rising Retirement Costs

Housing, energy bills, transport, and healthcare costs continue rising across the UK. Building additional savings before retirement can improve financial security later in life.

Stay Updated on Pension Changes

The government reviews pension rules regularly, meaning future increases to the state pension age UK remain possible. Following updates helps caregivers make informed decisions about retirement timing and savings goals.

For many care workers, retirement planning now starts years before reaching pension age. The earlier you prepare, the easier it becomes to manage the transition from full-time caregiving into retirement.

Conclusion

Understanding the changing state pension age UK rules has become increasingly important for caregivers and care workers across the country. Many women working in care roles now face longer working years, changing retirement expectations, and growing financial pressures later in life.

Whether you are checking the retirement age UK for female workers, reviewing your pension forecast, or planning for retirement after years in caregiving, taking action early can help you make more confident financial decisions.

Care workers dedicate their careers to supporting others, but many forget to plan properly for their own future. Reviewing your National Insurance contributions, workplace pension, and retirement timeline today can help you avoid unexpected challenges later.

At Care Sync Experts, we support care providers and caregivers with practical guidance, compliance support, workforce insights, and resources designed specifically for the UK care sector. Explore more expert articles and updates to stay informed about the changes affecting care professionals across the UK.

FAQ

When did women’s retirement age change from 60 to 65 in the UK?

The UK government began increasing women’s State Pension age in 2010 following the Pensions Act 1995. The changes gradually raised the pension age from 60 to 65 to match men’s retirement age. The transition completed in November 2018 before the pension age later increased further to 66.

Can I claim UK State Pension if I live abroad?

Yes, many people can still claim their UK State Pension while living abroad if they qualify through National Insurance contributions. However, annual pension increases may depend on the country where you live. Some countries receive yearly increases under UK agreements, while others do not.

Will my wife get a State Pension if she never worked?

In some cases, yes. A woman who never worked may still qualify for a State Pension through National Insurance credits, child benefit claims, caring responsibilities, or contributions linked to a spouse or civil partner under older pension rules. The exact amount depends on her individual circumstances and contribution history.

What is the new retirement age in 2026 in the UK?

The State Pension age in the UK remains 66 for most people in 2026. However, the government continues gradually moving toward a pension age of 67 for people born on or after April 6, 1961. Your exact retirement age depends on your date of birth.