Where Care Excellence Meets Business Success. Transform your operations today - 0333 577 0877

Log in to CareSync Interview Preparation.

UK State Pension Age Increase 2026:

What Care Businesses Need to Know

Text to speech

Duration: 00:00

Font size

Published: 9 Apr, 2026

Share this on:

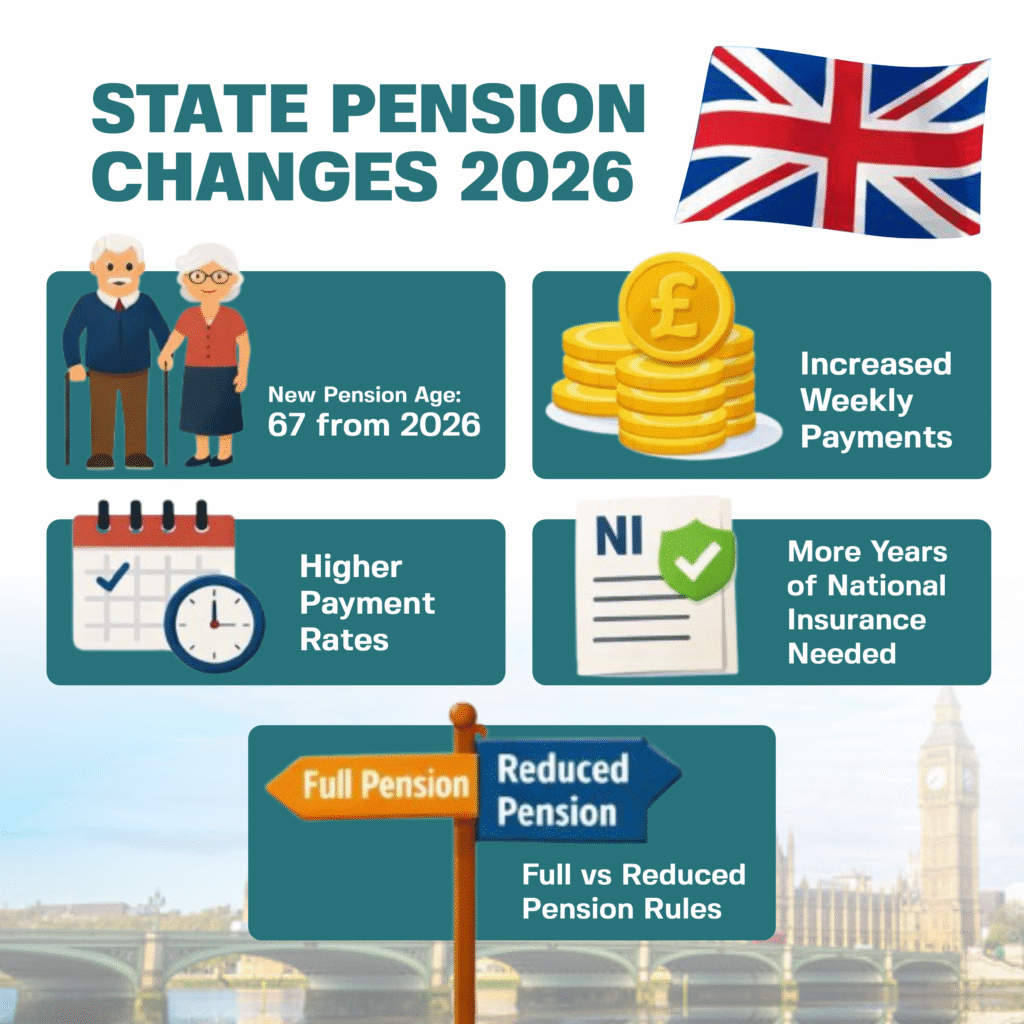

The UK State Pension age increase 2026 will raise the retirement age from 66 to 67 between April 2026 and April 2028. This change affects people born on or after 6 April 1960, meaning they will retire at age 67 instead of 66, depending on their exact birth date. The government introduced this state pension age increase to reflect longer life expectancy and reduce long-term pension costs.

If you’re asking “when can I retire?”, the answer now depends on your date of birth. The increase does not apply all at once, it rolls out gradually over two years, so some people will wait a few extra months, while others will wait the full year.

For care providers and their staff, this means many workers will remain in employment longer, making it essential to understand how the UK state pension age increase 2026 affects retirement planning and workforce decisions.

Key Takeaways

- The UK state pension age increase 2026 will raise the retirement age from 66 to 67 between April 2026 and April 2028.

- Anyone born on or after 6 April 1960 will reach state pension age later than expected.

- The change will affect when staff can retire at age 67, not 66, depending on their birth date.

- Care providers should expect longer staff retention, especially among experienced caregivers.

- You can confirm your exact retirement date using the UK State Pension age calculator on GOV.UK.

- Checking a state pension forecast helps employees understand how much they will receive and plan ahead.

- The state pension age increase will continue to shape workforce planning across the care sector.

Who Is Affected by the State Pension Age Increase in 2026?

The state pension age increase 2026 affects anyone born on or after 6 April 1960. If an employee falls into this group, they will not receive their State Pension at 66. Instead, they will need to wait until they reach age 67, depending on their exact birth date.

The increase does not apply equally to everyone. The government is rolling it out in phases between April 2026 and April 2028. For example, someone born in April 1960 may wait only a few extra months, while someone born later in the year could wait much longer.

From a caregiver business perspective, this change directly impacts your workforce:

- Many experienced caregivers will stay in employment longer

- Retirement timelines will become less predictable

- Workforce planning will require closer tracking of staff age and retirement expectations

The DWP state pension age change 2026 also means employers can no longer assume that staff in their mid-60s will retire soon. Instead, care providers should expect a gradual shift, where older employees remain active in the workforce for an extended period.

Understanding who is affected by the UK state pension age increase allows care businesses to plan staffing levels, manage expectations, and avoid sudden workforce gaps.

RELATED: What Is the Best Mobile Phone for Old Age UK in 2026?

When Can You Retire Now? (Use the Official Calculator)

If you’re asking “when can I retire?”, the answer now depends entirely on your date of birth. The state pension age increase 2026 means there is no single retirement age anymore; each person has a specific date.

The easiest way to check is by using the official UK State Pension age calculator on GOV.UK. This tool gives you your exact retirement date based on current legislation.

Quick Answer:

Your State Pension age depends on your date of birth, and you should use the official UK State Pension age calculator to confirm when you can retire.

How to check your pension age:

- Go to the GOV.UK pension calculator

- Enter your date of birth

- View your exact State Pension age and date

You can also check a state pension forecast to see how much you’re likely to receive under the New State Pension 2026 rules.

Caregiver businesses should encourage staff, especially those aged 55+, to use the UK State Pension calculator. This helps:

- Set realistic retirement expectations

- Prevent sudden staffing gaps

- Support better workforce planning

Because of the UK state pension age increase 2026 calculator results, two employees of the same age may now retire at different times. Care providers must account for this variation when planning schedules, hiring, and succession.

How Much Is the State Pension in 2026/27?

The state pension increase 2026/27 raises payments by 4.8%, in line with average earnings under the triple lock policy. This means higher weekly income for pensioners starting from April 2026.

Current Rates:

- New State Pension 2026:

£241.30 per week (£12,547.60 per year)

- Basic State Pension (pre-2016 retirees):

£184.90 per week (£9,614.80 per year)

The New State Pension in 2026 will pay up to £241.30 per week, depending on your National Insurance record.

To receive the full amount, individuals typically need 35 years of qualifying National Insurance contributions. Those with fewer years will receive a reduced amount.

How much is the state pension for a woman?

The amount is the same for men and women under the current system. What matters is the individual’s National Insurance record, not gender.

Understanding the state pension increase 2026 helps care businesses:

- Support staff with retirement planning

- Explain income expectations to older employees

- Reduce uncertainty around financial readiness

Many caregivers may rely heavily on the New State Pension 2026, especially if they do not have private pensions. Encouraging staff to check their state pension forecast ensures they understand what they will actually receive and whether they need to work longer.

READ MORE: What Time Is Sundowning? 2026 Update for Care Workers

What This Means for Caregiver Businesses

The UK state pension age increase 2026 will directly affect how care providers manage their workforce. As employees delay retirement, your staffing model will shift, both positively and negatively.

Quick Insight:

The state pension age increase means more experienced caregivers will stay in the workforce longer, but it also increases the risk of burnout and workforce imbalance.

1. Longer Staff Retention

Many caregivers who planned to retire at 66 will now continue working until 67.

This can benefit your business:

- You retain experienced staff longer

- You reduce short-term recruitment pressure

- You maintain continuity of care for clients

2. Increased Burnout Risk

Older caregivers may:

- Struggle with physically demanding roles

- Experience fatigue or reduced mobility

This creates a real operational risk if not managed properly.

3. Workforce Planning Becomes Critical

The UK pension age reform impact means you must actively plan for:

- Gradual retirement timelines

- Flexible working options

- Succession planning

You can no longer assume when staff will leave. Instead, you must track and manage retirement expectations.

4. Recruitment Strategy Must Evolve

With delayed retirement:

- Fewer roles may open up immediately

- Younger workers may face slower entry into the sector

Care providers should balance:

- Retaining experienced staff

- Bringing in new talent

What smart care providers are doing

Forward-thinking providers are already:

- Offering flexible shifts for older staff

- Reducing physically demanding tasks

- Encouraging staff to check their state pension forecast

- Staying updated with pension news and DWP changes

The state pension age increase is not just a policy change, it is a workforce shift. Care providers who adapt early will maintain stability, reduce risk, and stay competitive.

SEE ALSO: Will a Bladder Infection Cause Nausea UTI? A Caregiver’s Guide (2026)

Should Care Providers Adjust Workforce Planning Now?

Yes, care providers should start adjusting workforce planning now. The state pension age increase 2026 will delay retirement for many employees, which changes how you manage staffing, scheduling, and long-term growth.

Care providers should adjust workforce planning now if they rely on older staff, because the state pension age increase will delay retirement and change workforce availability.

When you SHOULD adjust now

You should act immediately if:

- A large portion of your workforce is aged 55+

- You rely heavily on experienced caregivers

- You expect staff to retire soon based on old assumptions

In these cases, the state pension age increase will directly affect your staffing timeline.

When adjustment is less urgent

You may not need immediate changes if:

- Your workforce is mostly younger (under 50)

- You already have strong recruitment pipelines

- You use flexible or agency staffing models

Practical steps care providers should take

To adapt effectively:

- Review staff age profiles and expected retire at age timelines

- Encourage employees to check when can I retire using official tools

- Offer flexible roles for older staff

- Introduce succession planning early

- Train younger staff to prepare for future leadership roles

The risk of doing nothing

If you ignore the state pension age increase 2026, you may face:

- Unexpected staff shortages

- Burnout among older employees

- Poor workforce planning decisions

The state pension age increase is already underway. Care providers who respond early will maintain stability, support their staff better, and avoid operational disruptions.

MORE: CQC Registration for Domiciliary Care Providers: Complete 2026 Guide

Future Pension Changes You Should Watch (2025–2046)

The state pension age increase 2026 is only one part of a wider shift in UK pension policy. Care providers should stay informed about upcoming changes, because these updates will continue to affect workforce planning and staff expectations.

Quick Insight:

The UK government plans to increase the State Pension age to 68 in the future, and ongoing policy reviews could bring further changes.

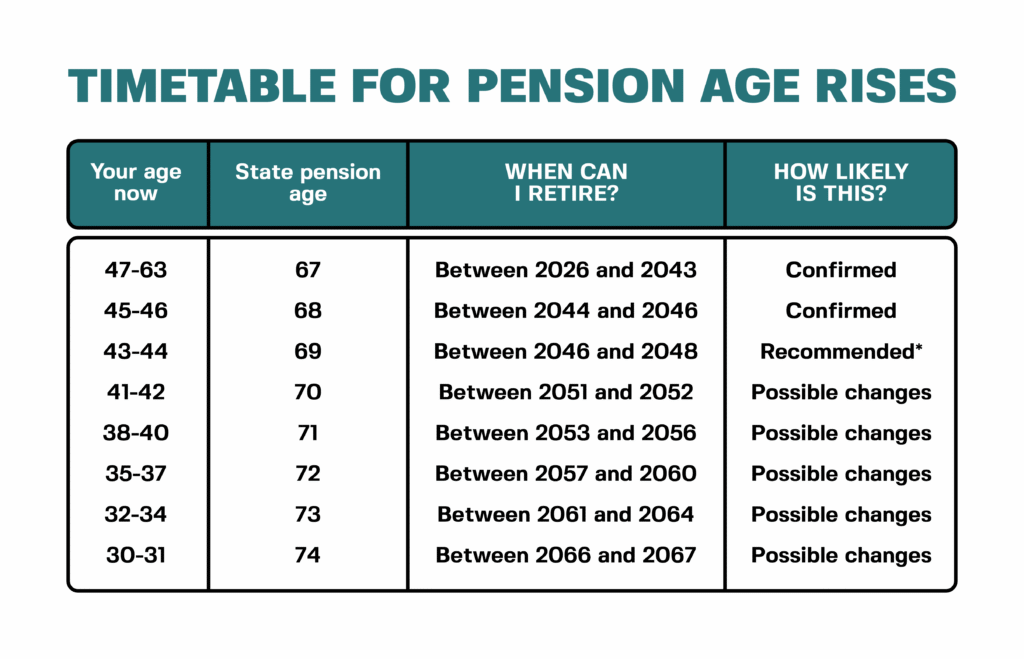

1. Planned Increase to Age 68

The government has already scheduled another state pension age increase:

- Age 68 is expected between 2044 and 2046

- Future reviews may bring this forward depending on life expectancy and economic conditions

This means younger caregivers may need to work even longer before they retire at age.

2. Ongoing Reviews and DWP Updates

The Department for Work and Pensions (DWP) regularly reviews pension policy. Recent pension news highlights:

- Potential adjustments based on life expectancy trends

- Discussions around affordability and sustainability

- Occasional DWP state pension warnings about planning ahead

Care providers should monitor these updates to avoid being caught off guard.

3. Other Pension Changes to Watch

Several related updates may also impact your staff:

- UK pensioner cash withdrawal changes 2025 – potential changes in how pension funds are accessed

- UK state pension reduction 2025 – concerns around reduced real value due to inflation or policy shifts

- September 2025 state pension updates – periodic policy announcements affecting benefits

These changes may influence how employees view retirement and financial security.

Understanding future pension trends helps you:

- Prepare for long-term workforce changes

- Support staff with realistic retirement expectations

- Stay aligned with UK pension age reform impact

The UK state pension age increase will continue evolving. Care providers who stay informed and adapt early will remain stable, competitive, and better prepared for future workforce challenges.

READ: What is an SR1 Form? 2026 Guide for UK Care Providers

Common Questions About the UK State Pension Age Increase 2026

When will the State Pension age reach 67?

The state pension age increase 2026 will raise the retirement age from 66 to 67 between April 2026 and April 2028. The change happens gradually, so not everyone reaches 67 at the same time.

Can I still retire at 66?

Yes, you can still retire at 66, but you may not receive your State Pension yet. If you fall under the UK state pension age increase, you will need to wait until your official pension age before receiving payments.

How do I check when I can retire?

You should use the official UK State Pension age calculator.

Your exact retirement age depends on your date of birth, and the calculator provides the most accurate answer.

You can also check your state pension forecast to understand how much you’ll receive.

Will the State Pension age increase again?

Yes. The government has already planned another state pension age increase to 68 between 2044 and 2046, although future reviews may change this timeline.

What happens if I don’t have enough National Insurance contributions?

You may receive less than the full New State Pension 2026 amount. To qualify for the full payment, you typically need 35 years of contributions. If you have gaps, you may still qualify for a partial pension.

Does the State Pension amount differ for men and women?

No. The amount is the same for both. The key factor is your National Insurance record, not gender.

If you’re wondering how much is the state pension for a woman, the answer is the same as for men under the current system.

These questions reflect the most common concerns around the UK state pension age increase 2026. Clear answers help both individuals and care providers plan more effectively.

Conclusion

The UK state pension age increase 2026 is more than a policy update—it’s a workforce shift that care providers must manage proactively.

What you should do now:

- Expect staff to retire at age 67, not 66

- Encourage employees to check when can I retire using the UK State Pension age calculator

- Support staff in reviewing their state pension forecast

- Adjust workforce planning to reflect delayed retirement

- Introduce flexible roles to reduce burnout among older caregivers

- Stay updated with pension news and DWP state pension age change 2026 developments

Care providers who understand the state pension age increase early will manage staffing better, retain experienced workers, and avoid sudden workforce gaps.

The state pension age increase 2026 is already shaping the future of the care sector. By acting now, you can protect your workforce, support your staff, and keep your operations stable in a changing environment.

Need Support Managing Workforce Changes from the State Pension Age Increase?

The UK state pension age increase 2026 can disrupt staffing plans, delay retirements, and increase pressure on your existing team if not managed early.

Care Sync Experts helps you:

- Plan for delayed retirement and workforce shifts

- Retain experienced caregivers without increasing burnout

- Build flexible staffing models that support older employees

- Improve workforce stability and reduce sudden staff shortages

- Stay aligned with regulatory expectations and long-term care demands

Book a Free Workforce Strategy Consultation

Get practical, expert guidance to adapt your care service, support your staff, and stay ahead of pension-related workforce changes.

FAQ

Do I get my husband’s State Pension if he dies?

You may be able to receive part of your husband’s State Pension, depending on your circumstances. This is usually called inheriting State Pension or qualifying for bereavement benefits.

– If you reached State Pension age before April 2016, you may inherit some of your partner’s pension based on their National Insurance record.

– If you’re under the new State Pension system (after April 2016), inheritance is more limited, but you may still qualify for Bereavement Support Payment (BSP).

The exact amount depends on contributions, age, and marital status.

How long is pension paid after death in the UK?

State Pension payments stop shortly after death. However:

– Payments may continue briefly if they were already issued before the death was reported

– Any overpayments must usually be returned

– A surviving spouse or partner may qualify for bereavement benefits instead

You should report a death to the DWP immediately to avoid complications.

Can I pass my pension to my children?

You cannot pass your State Pension directly to your children. The State Pension is not treated as a transferable asset.

However:

– Private or workplace pensions can often be passed on, depending on the scheme

– Beneficiaries may receive lump sums or ongoing payments

Always check the specific rules of your pension provider.

What is the minimum salary to qualify for State Pension in the UK?

There is no fixed minimum salary to qualify for the State Pension. Instead, eligibility depends on National Insurance (NI) contributions.

– You typically need at least 10 qualifying years to receive any pension

– You need 35 years to receive the full New State Pension 2026

You earn qualifying years by:

– Working and paying NI contributions

– Receiving NI credits (e.g., for caregiving, unemployment, or illness)

Even low earners can qualify, as long as they meet the contribution requirements.

Would you like to receive update from CareSync Experts?

All rights reserved. Copyright © - Care Sync Experts.