Where Care Excellence Meets Business Success. Transform your operations today - 0333 577 0877

Log in to CareSync Interview Preparation.

Universal Credit Permanent Boost 2026

Text to speech

Duration: 00:00

Font size

Published: 8 Jun, 2026

Share this on:

The Universal Credit permanent boost increased the basic monthly amount claimants receive through the Universal Credit standard allowance from April 2026.

The current monthly rates are £338.58 for single claimants under 25, £424.90 for single claimants aged 25 or over, £528.34 for joint claimants both under 25, and £666.97 for joint claimants where either person is 25 or over.

For carers and families, this rise matters because many vulnerable people already stretch their income across food, bills, transport, disability costs, appointments, and daily support. A higher standard allowance can ease some pressure, but it does not tell the full story.

The Universal Credit boost 2026 affects the basic allowance first. A person’s final payment still depends on their rent, children, earnings, savings, deductions, health status, and caring responsibilities. So, when families ask how much is UC going up in April 2026, they should check both the new standard allowance and the full award breakdown.

The government says the wider reform will raise the standard allowance above inflation for several years, with the increase worth an estimated £725 by 2029/30 for a single adult aged 25 or over.

What Is the £725 Universal Credit Boost?

The £725 Universal Credit boost is not a one-off lump sum that everyone receives in their bank account. It describes the estimated yearly gain by 2029/30 for a single claimant aged 25 or over, compared with what they would have received if the standard allowance only rose with inflation.

This means the Universal Credit boost payment works through higher monthly standard allowance rates, not through a separate “cost of living” style payment.

For carers and families, that distinction matters. If someone you support expects one large payment, they may plan their budget wrongly. The increase comes through their normal Universal Credit award, so they should check their monthly statement to see how the new rate affects them.

The Universal Credit Act supports this above-inflation rise over several years. In simple terms, the government wants to lift the basic Universal Credit rate while also changing parts of the wider welfare system. So the headline figure sounds simple, but each claimant’s real monthly payment still depends on their full circumstances.

RELATED: What Is the Carers Element Universal Credit? 2026

Why the Universal Credit Act Changed the Standard Allowance

The Universal Credit Act changed the way the Universal Credit standard allowance rises from 2026. Instead of only increasing in line with inflation, the standard allowance will rise above inflation for several years, from 2026/27 to 2029/30. The government describes this as the first sustained above-inflation uplift to the basic UC rate.

The aim is to raise the core monthly payment while reshaping parts of the wider welfare system. The welfare bill Universal Credit reforms also included changes to health-related UC support, including a reduced health top-up for some new claims from April 2026.

For carers and families, the key point is simple: the Universal Credit Bill UK changes may increase the basic allowance, but they do not guarantee the same final payment for everyone. A claimant’s actual UC award still depends on rent, children, earnings, savings, deductions, disability status, health elements, and caring responsibilities.

So families should not stop at the headline boost. They should check the full Universal Credit statement and make sure every relevant element appears correctly.

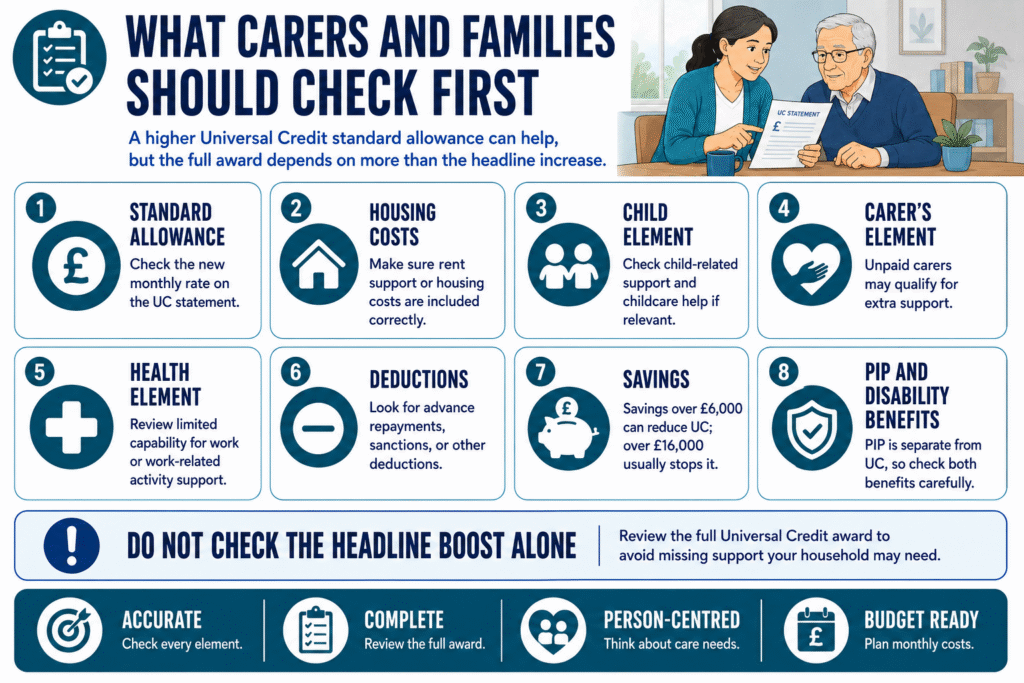

What Carers and Families Should Check First

A higher Universal Credit standard allowance can help, but carers should still check the full award. Universal Credit includes different elements, and one missing detail can reduce the money someone receives each month.

If you support someone on UC, check these first:

- Their new standard allowance

- Housing costs or rent support

- Child element and childcare support

- Carer’s Element, if someone provides regular unpaid care

- Limited capability for work or work-related activity

- Advance repayments, sanctions, or deductions

- Work income

- Savings, investments, or other capital

- Disability benefits, including PIP

Families often ask, does Universal Credit affect PIP? Universal Credit and PIP serve different purposes. PIP supports people with daily living or mobility needs, while UC supports people on a low income or out of work. A person may receive both, depending on their circumstances.

Carers should also check savings. If someone asks, can Universal Credit check my savings account or how much savings are you allowed on Universal Credit, the key rule is that savings over £6,000 can reduce UC, and savings over £16,000 usually mean the person cannot get UC. GOV.UK says UC reduces by £4.35 for every £250 between £6,000 and £16,000.

READ MORE: Is Carers Allowance Taxable in 2026?

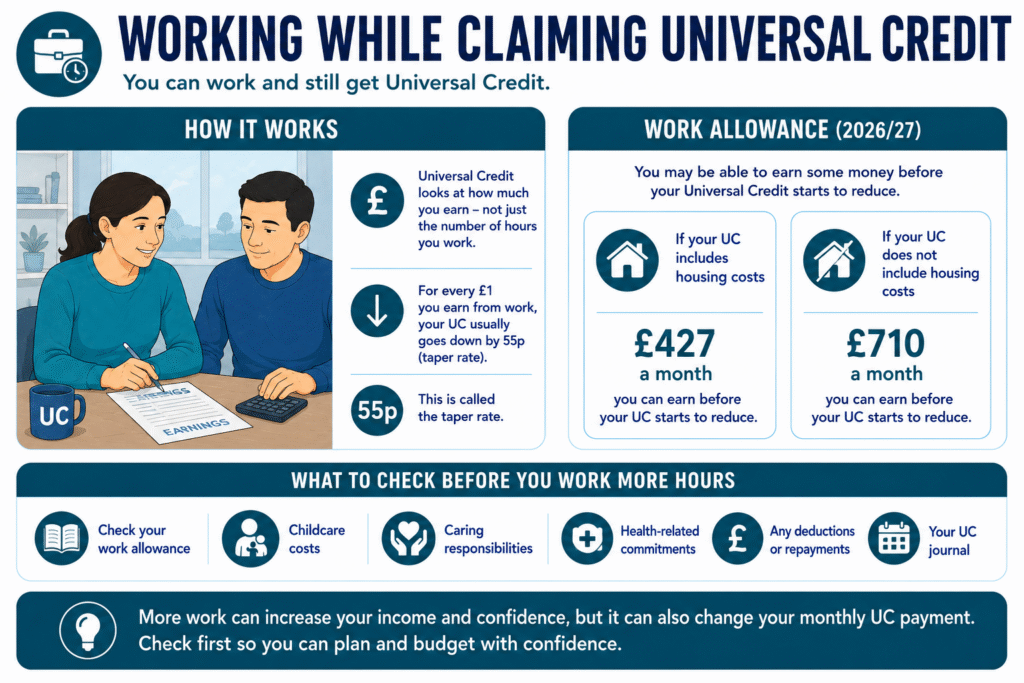

Working While Claiming Universal Credit

Universal Credit does not set one fixed number of hours everyone can work. Instead, it looks at how much someone earns, whether they qualify for a work allowance, and how the taper rate reduces their payment as earnings rise.

So, when families ask how many hours can you work on Universal Credit, the better question is: how much will the person earn, and how will that affect their monthly award?

Some people can work part-time and still receive Universal Credit. This often matters for carers, disabled claimants, and people trying to return to work gradually after illness. The payment may reduce as earnings increase, but work does not always mean UC stops immediately.

If someone you support wants to increase their hours, start a new job, or try work after a health problem, check their Universal Credit journal, work allowance, childcare costs, and any health-related commitments first. A small change in earnings can affect rent support, deductions, and the final amount paid into their bank account.

Working While Claiming Universal Credit

You can work and still claim Universal Credit. There is no single answer to how many hours can you work on Universal Credit, because UC looks at how much you earn, not just how many hours you work.

For every £1 you earn from work, your Universal Credit usually goes down by 55p. GOV.UK calls this the taper rate. If you have children or a health condition that affects your ability to work, you may also get a work allowance, which lets you earn a set amount before your UC starts to reduce. In 2026/27, that work allowance is £427 a month if UC includes housing costs, or £710 a month if it does not.

For carers and families, this matters when someone wants to try part-time work, return after illness, or increase their hours. More work can improve confidence and income, but it can also change the monthly UC payment.

Before changing hours, check the person’s UC journal, work allowance, childcare costs, caring responsibilities, and health-related commitments. That helps the family plan properly instead of guessing how the change will affect their budget.

SEE ALSO: Early Sign of MND in 2026: What Care Businesses Should Notice First

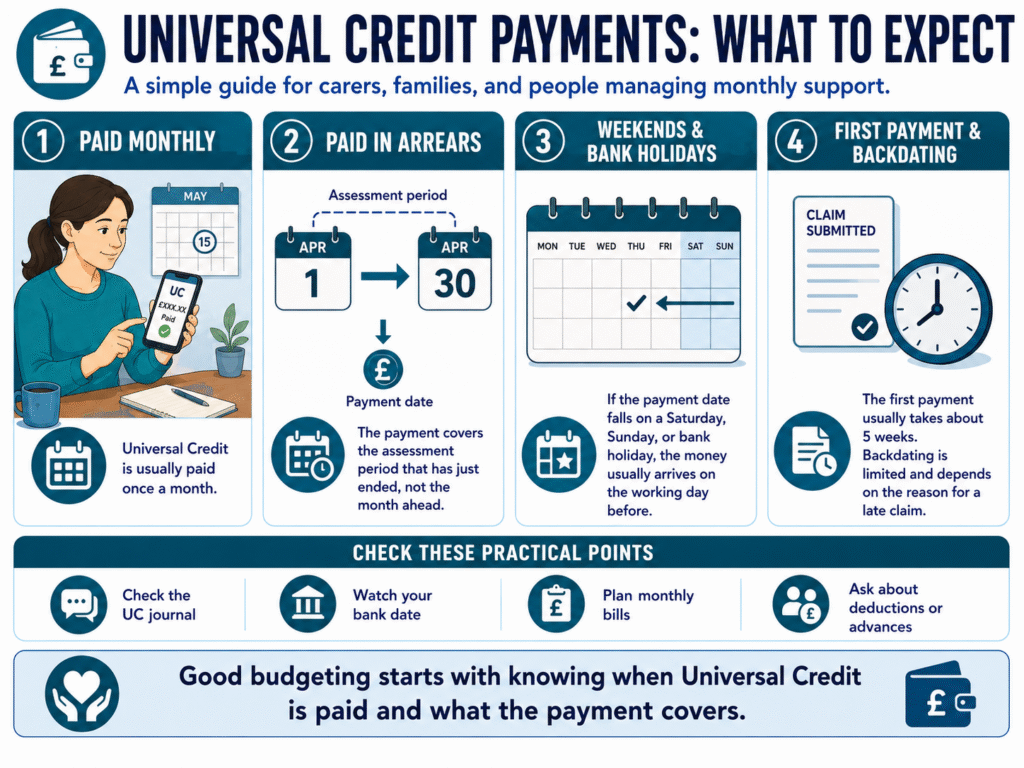

Payments, Arrears, Weekends and Backdating

Universal Credit is usually paid once a month, in arrears. This means the payment covers the assessment period that has just ended, not the month ahead. For carers and families, this matters because the person you support may need help budgeting between payment dates.

GOV.UK says Universal Credit claimants usually receive their first payment around five weeks after making a claim, and later payments arrive on the same date each month. If the payment date falls on a weekend or bank holiday, the payment usually arrives on the working day before.

So, if someone asks do Universal Credit pay on a Saturday, the answer is usually no. If the due date falls on a Saturday, Sunday, or bank holiday, the money normally comes earlier.

Many people also ask what time does Universal Credit get paid into bank. Banks process payments at different times, so the exact time can vary. Check the UC online account first, then check the bank account later in the day if the payment has not appeared.

Backdating works differently. If someone asks how long does it take to get backdated Universal Credit, they should know that backdating is limited and depends on why the claim started late. A carer should help the person explain the reason clearly in their UC journal and keep evidence where possible.

Savings, Home Ownership, Travel and Stopping a Claim

Universal Credit is means-tested, so savings and capital can change what someone receives. If the person you support has savings between £6,000 and £16,000, their UC will reduce. If they have over £16,000, they usually cannot claim Universal Credit. GOV.UK says UC reduces by £4.35 for every £250 of capital between £6,000 and £16,000.

Families also ask, can you get Universal Credit if you own a house? Yes, owning the home you live in does not automatically stop a UC claim. However, other property, savings, or capital can affect entitlement. Homeowners may also qualify for Support for Mortgage Interest, but GOV.UK treats this as a loan that must usually be repaid with interest when the home is sold or transferred.

If someone asks how long can you go abroad on Universal Credit, the general rule is up to one month, as long as they remain eligible and tell their work coach before going. GOV.UK says UC cannot continue if someone moves abroad permanently.

A claimant can also ask to close their UC claim. But if someone asks, can I voluntarily stop Universal Credit, carers should help them check the impact first. Stopping a claim may affect rent support, council tax help, free prescriptions, budgeting, and future benefit access.

MORE: What Is Safeguarding in Care? 2026 Update

What About ESA, PIP and Disability Support?

Universal Credit does not replace PIP. If someone asks does Universal Credit affect PIP, the answer is usually no in the direct sense: PIP supports people with daily living or mobility needs, while Universal Credit supports people on a low income or out of work. A person can receive both if they qualify.

Carers should still look at the full picture. PIP can affect other parts of a household’s benefit situation, such as carer support, disability premiums in older benefits, or help linked to health needs. It can also strengthen the evidence that someone needs extra care, supervision, mobility support, or help with daily living.

Many families also ask how much is PIP going up in April 2026. PIP rates usually increase each tax year, so check the latest GOV.UK rates before budgeting around disability income.

If someone asks is ESA to Universal Credit delayed to 2028, they should check their official migration notice rather than rely on rumours. ESA and UC migration rules have changed over time, and the safest step is to read the letter, check the deadline, and get benefits advice before making a claim.

For carers, the main point is this: do not look at the Universal Credit permanent boost alone. Check UC, PIP, ESA, Carer’s Allowance, housing support, health elements, and deductions together before making care or household budget decisions.

Final Advice for Carers and Families

The Universal Credit boost 2026 can give many households more breathing space, but carers should not plan around the headline rise alone. The final payment still depends on the full Universal Credit award, not just the standard allowance.

If you support someone who depends on UC, check their monthly statement carefully. Look at their housing costs, children’s elements, Carer’s Element, health elements, work income, savings, deductions, and any advance repayments. A small change in one area can affect the money they actually receive.

The Universal Credit permanent boost may help with food, bills, travel, appointments, and daily living costs. But vulnerable people, disabled claimants, older adults, and unpaid carers often need more than a higher basic rate. They may also need disability support, proper care planning, benefits advice, and help managing their budget.

The safest approach is simple: check the full award, keep records, update changes quickly, and ask for advice before making big decisions about work, travel, savings, care costs, or stopping a claim.

Need Help Understanding Universal Credit and Care Support?

Universal Credit changes can affect household budgets, care decisions, and the support vulnerable people rely on.

At Care Sync Experts, we explain care, benefits, and family support in plain English, helping carers and families make confident, informed decisions.

Get practical guidance before money worries become care worries.

FAQ

Can Universal Credit give me extra money?

Yes. Universal Credit may offer extra help through an advance payment, a budgeting advance, a hardship payment, or other financial support if you need help with bills or unexpected costs.

An advance is not free money; you usually repay it through future Universal Credit payments. GOV.UK says budgeting advances are normally repaid through UC over 24 months.

What free things can you get on Universal Credit?

Universal Credit can help you qualify for extra support, depending on your income, household and location. This may include help with NHS prescriptions, dental care, eye tests, school meals, childcare costs, housing costs, council tax support, and local crisis support.

GOV.UK also confirms that free school meals eligibility in England is expanding to include children from households receiving Universal Credit from the 2026/27 school year.

Will UC get a Christmas Bonus?

Universal Credit on its own does not qualify someone for the Christmas Bonus. The Christmas Bonus is a separate one-off £10 tax-free payment for people who receive certain qualifying benefits during the qualifying week, usually the first full week of December. If someone only gets Universal Credit, they should not assume they will get it automatically.

Do you have to pay Universal Credit back?

You do not usually pay back normal Universal Credit entitlement if the award is correct. But you may have to repay advance payments, budgeting advances, overpayments, or benefit debt. GOV.UK says that if you owe benefit money while getting UC, your benefit payments can reduce until you repay it.

Would you like to receive update from CareSync Experts?

All rights reserved. Copyright © - Care Sync Experts.