Where Care Excellence Meets Business Success. Transform your operations today - 0333 577 0877

Log in to CareSync Interview Preparation.

What Is the Retirement Age in the UK? (2026 Guide for Care Workers & Providers)

Text to speech

Duration: 00:00

Font size

Published: 20 Mar, 2026

Share this on:

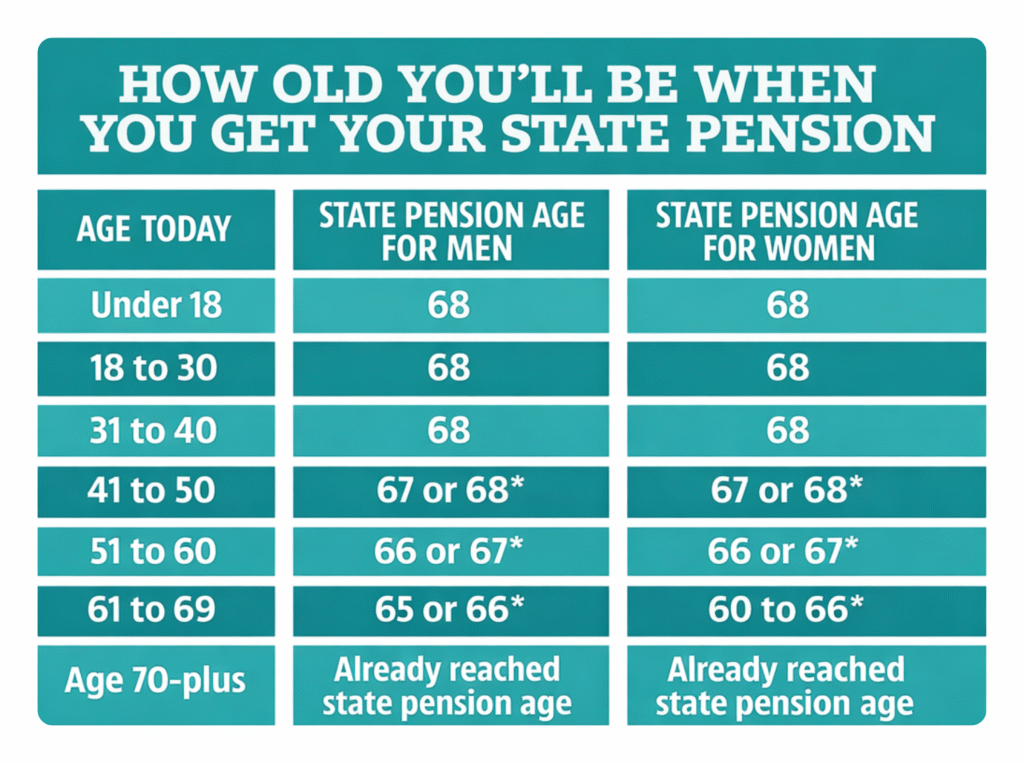

The UK State Pension age is currently 66. The government is increasing it to 67 for people born on or after 6 April 1961, with the full change in place by 2028. A further rise to 68 is planned between 2044 and 2046, but officials may review this timeline.

So if you’re asking, “is state pension age 66 or 67?”, the answer depends on your date of birth. Some people will retire at 66, while others will retire at 67 as the transition continues.

The government has already confirmed these updates as part of ongoing UK state pension age retirement changes, driven by longer life expectancy and economic pressure on the pension system.

For private and workplace pensions, the minimum access age is currently 55, but it will increase to 57 from April 2028.

Key facts at a glance:

- Current State Pension age: 66

- Rising to: 67 by 2028

- Future proposal: 68 (2044–2046, under review)

- Private pension access: 55 → 57 (from 2028)

This means the answer to “what is the retirement age in the UK?” is no longer fixed; it depends on when you were born and the ongoing changes set by the government.

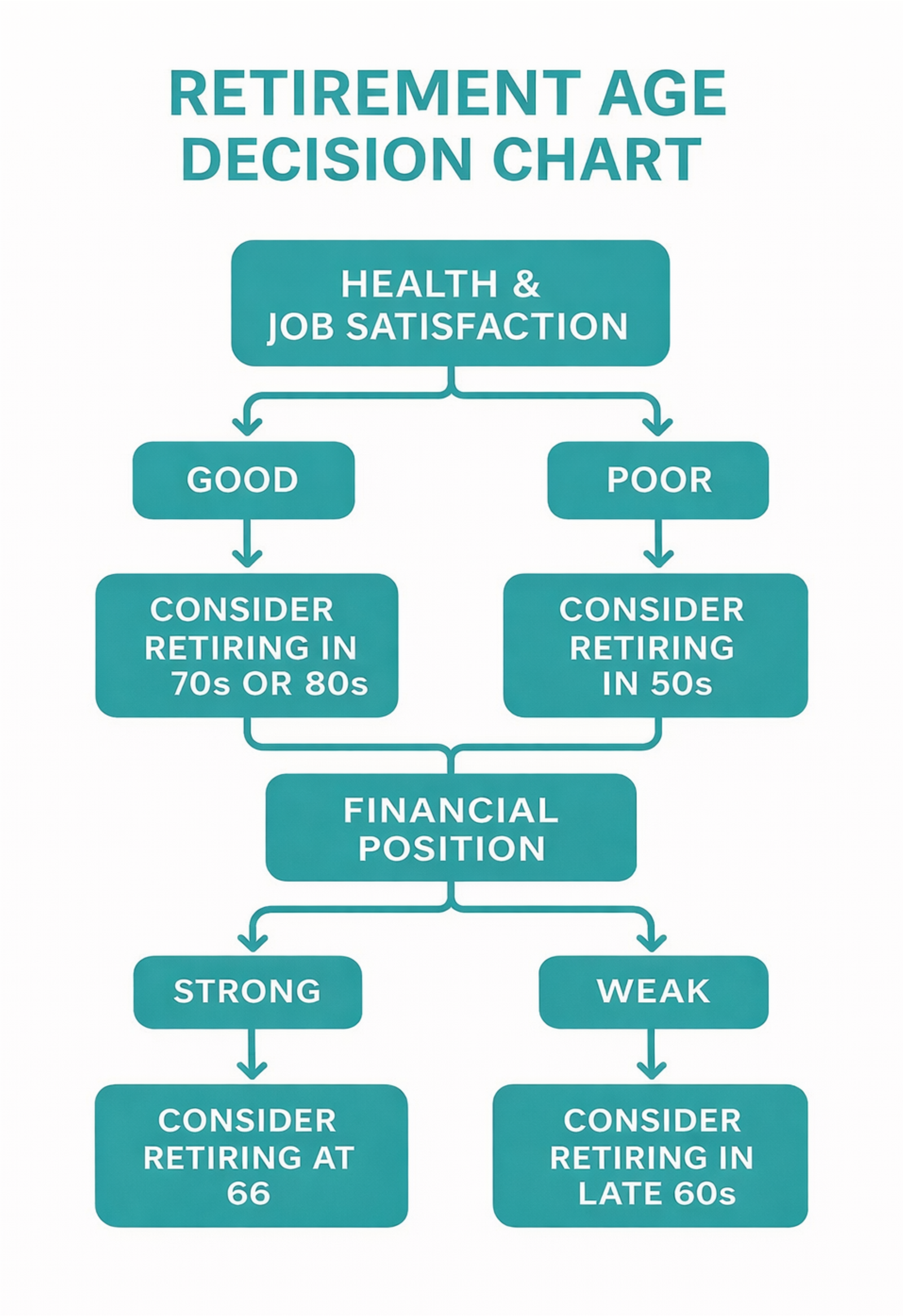

When Can I Retire in the UK?

You can retire at any age in the UK, but you can only claim your State Pension once you reach the official State Pension age.

This means:

- Retirement age ≠ State Pension age

- You can stop working earlier, but you must fund it yourself until your pension starts

So if you’re asking “when can I retire?”, the real answer is: You can retire whenever you choose, but you can only access your State Pension at 66–67 (depending on your age group).

What Happens If You Retire Early?

Many people, especially in physically demanding roles like caregiving, choose to retire before State Pension age. However:

- You will not receive your State Pension yet

- Your income must come from:

- Private or workplace pensions

- Personal savings

- Other investments

If you retire too early without a plan, you risk a significant income gap.

Can You Keep Working After Retirement Age?

Yes, and many people do.

There is no forced retirement age in the UK anymore. You can:

- Keep working full-time or part-time

- Claim your State Pension while working

- Increase your pension if you delay claiming it

What This Means for Care Workers

Care work is physically and emotionally demanding. Many carers aim to retire earlier, but in reality:

- Most must keep working until at least 66–67

- Financial pressure often delays retirement

- Proper planning becomes critical

In simple terms, you can retire at any age, but you can only comfortably retire when your income supports it.

UK State Pension Age Changes Explained (Timeline)

The UK government has already confirmed several state pension age increases, and these changes affect exactly when you can retire and claim your pension.

If you’re wondering about the UK state pension age increase in 2026 or beyond, the key point is this: The increase to age 67 is already in progress; it is not a future proposal, it is happening now in phases.

State Pension Age by Date of Birth

| Date of Birth | State Pension Age |

| Before 6 April 1960 | 66 |

| 6 April 1960 – 5 March 1961 | 66 (plus gradual monthly increases) |

| 6 March 1961 – 5 April 1977 | 67 |

| After April 1977 | 68 (planned, under review) |

What Does “Phased Increase” Mean?

The transition from 66 to 67 is gradual, not instant.

If you were born between:

- April 1960 and March 1961, your pension age increases month by month

- After that, it settles at 67

This is why two people just months apart in age may retire at different times.

Has the Government Changed the Retirement Age?

Yes, and it continues to review it regularly.

The Department for Work and Pensions (DWP) reviews pension age based on:

- Life expectancy trends

- Economic sustainability

- Workforce participation

This is part of the ongoing government state pension age review, which means future changes remain possible.

What About the 2026 Pension Age Increase?

There is no sudden jump happening specifically in 2026.

Instead:

- The increase to 67 is already being rolled out gradually

- By 2028, everyone affected will retire at 67

Many people search for “DWP state pension age change 2026”, but in reality, 2026 sits within an ongoing transition, not a single change point.

RELATED: What Disabilities Qualify for Council Tax Reduction? 2026

Why Is the State Pension Age Increasing?

The UK government is increasing the State Pension age because people are living longer and the pension system must stay financially sustainable.

This is not a one-time decision; it is part of an ongoing state pension age review carried out by the government.

The Three Main Reasons Behind the Increase

1. People Are Living Longer

Life expectancy has improved significantly over the years.

This means:

- People spend more years in retirement

- The government pays pensions for longer periods

Without changes, the system becomes too expensive to maintain.

2. Rising Cost of State Pensions

The State Pension is funded through taxes and National Insurance contributions.

As more people retire:

- Fewer workers support more retirees

- Government spending on pensions increases

The state pension age increase helps balance this pressure.

3. Workforce Sustainability

The government wants more people to:

- Stay in work longer

- Contribute to the economy

- Reduce pressure on public finances

This is why you see ongoing UK state pension age increases rather than a fixed retirement age.

What the Government Review Means

The government state pension age review looks at:

- Life expectancy data

- Economic conditions

- Public spending

This is why future changes, like the increase to 68, remain under review and not fully locked in.

What This Means for Care Workers

This change hits care workers harder than most.

Care roles are:

- Physically demanding

- Emotionally exhausting

- Often lower paid

Yet many carers must now:

- Work longer than previous generations

- Delay retirement plans

- Rely more on personal savings

In practice, many care workers cannot easily continue working into their late 60s, which makes early financial planning essential.

READ MORE: Bereavement Support Payment (BSP) in the UK: Who Qualifies, How Much You Get, and How to Apply

Will the Pension Age Increase to 68?

Yes, the UK government plans to increase the State Pension age to 68, but this change is not final and remains under review.

What Is Currently Planned?

- The State Pension age is expected to rise to 68 between 2044 and 2046

- This mainly affects people born after April 1977

However, this timeline could change depending on future government decisions.

Is Pension Age 67 Being Phased Out?

No, the opposite is happening.

- Age 67 is being phased in, not removed

- By 2028, it will fully replace 66 for those affected

So if you’ve seen searches like “pension age 67 phased out”, that is incorrect.

Why the Uncertainty Around Age 68?

The government reviews pension age regularly through the state pension age review process.

They look at:

- Life expectancy trends

- Economic conditions

- Public spending sustainability

If people stop living longer at the same rate, the increase to 68 could be delayed.

What This Means for You

- If you are under 45–50 today, you may retire at 68 instead of 67

- If you are older, your pension age is more likely already fixed at 66 or 67

What This Means for Care Workers

For those working in care:

- Working until 68 may not be realistic for many

- Physical demands make long careers harder

- Financial planning becomes even more important

Many carers will need to plan for alternative retirement strategies, not just rely on the State Pension.

Retirement Age UK. Male vs Female (Is There a Difference?)

There is no longer a difference between the retirement age for men and women in the UK.

Today:

- Retirement age UK for female = same as male

- Both follow the same State Pension age rules (66 → 67 → 68)

When Did the Retirement Age Change from 60 to 65 in the UK?

Historically:

- Women could claim State Pension at 60

- Men claimed at 65

The government gradually equalised pension ages between 2010 and 2018, bringing women’s pension age up to match men’s.

After that:

- Both increased together from 65 to 66

- Now both are moving to 67

Why Did the Government Equalise Retirement Age?

The government made this change to:

- Ensure fairness between men and women

- Reflect longer life expectancy

- Maintain economic sustainability

What This Means Today

If you’re asking:

- “Retirement age UK for female?”

- “Retirement age UK for male?”

The answer is the same: Your retirement age depends on your date of birth, not your gender.

Important Clarification

Some people still assume:

- Women retire earlier

- Different pension rules apply

This is no longer true.

All current and future UK state pension age increases apply equally to everyone.

SEE ALSO: NHS Hearing Aids UK: Cost, Types, Waiting Times, and How to Get One in 2026

How Much Is the UK State Pension?

The full UK State Pension is currently up to £221.20 per week (2024/2025 rate). This equals roughly £11,500 per year, but the exact amount you receive depends on your National Insurance record.

What Determines How Much You Get?

To receive the full State Pension, you usually need:

- 35 years of National Insurance contributions

- At least 10 qualifying years to receive anything at all

If you have fewer than 35 years:

- Your pension amount will be reduced proportionally

Can You Increase Your State Pension?

Yes , you can increase your pension by:

- Continuing to work and pay National Insurance

- Making voluntary contributions to fill gaps

- Delaying (deferring) your pension, which increases weekly payments

Is the State Pension Enough to Retire On?

For many people, the answer is no.

If you’re asking:

- “How much is state pension UK?”

- “How much do I need to retire?”

The State Pension alone usually provides basic income, not full financial security.

What This Means for Care Workers

Many care workers:

- Earn modest wages

- Rely heavily on the State Pension

- Have limited private pension contributions

This makes it even more important to:

- Plan early

- Consider workplace pensions

- Avoid relying only on the State Pension

Private & Workplace Pension Age (Important Change)

The State Pension age is not the same as when you can access your private or workplace pension.

Right now:

- You can usually access private pensions from age 55

However, this is changing.

What Is Changing in 2028?

From 6 April 2028:

- The minimum pension access age will increase from 55 to 57

This change aligns with the wider UK state pension age increase, ensuring people do not rely too early on pension savings.

Are There Any Exceptions?

Yes, some people may still access pensions earlier if:

- They have protected pension ages (from older schemes)

- They retire due to serious ill health

Always check with your pension provider for specific rules.

Why This Change Matters

If you’re planning to retire early, this change directly affects you.

For example:

- You may need 2 extra years of savings

- Early retirement becomes more difficult without proper planning

What This Means for Care Workers

For many care workers:

- Early retirement is common due to the physical nature of the job

- But the increase to 57 delays access to pension funds

- This creates a bigger gap between stopping work and receiving income

Without planning, this gap can become financially stressful.

MORE: Children’s DLA Rates: Who Qualifies, and What to Claim in 2026

What Happens at Age 66? (Benefits, Work & Income)

Turning 66 is a major milestone because it is currently the point when most people reach their State Pension age.

But many people ask: Do benefits vanish at 66? The answer is not exactly, but things do change.

What You Gain at Age 66

Once you reach State Pension age, you can:

- Start receiving your State Pension

- Stop paying National Insurance contributions

- Access certain age-related benefits (if eligible)

What Changes or Stops

Some benefits may stop or change when you reach State Pension age:

- Working-age benefits (like Universal Credit) may stop or transition

- You may instead qualify for:

- Pension Credit

- Other age-related support

This is why people often say “benefits vanish at 66,” but in reality, they shift rather than disappear.

Can You Still Work at 66?

Yes, and many people do.

At 66:

- You can continue working full-time or part-time

- You can receive your State Pension while working

- You may still need to pay income tax, depending on total earnings

The UK no longer has a fixed retirement age, so you decide when to stop working.

Should You Claim Your Pension Immediately?

You don’t have to.

If you delay claiming your State Pension:

- Your payments will increase later

- This is known as deferring your pension

What This Means for Care Workers

For care workers:

- Many continue working past 66 due to financial needs

- Others reduce hours instead of fully retiring

- The physical nature of care work makes this decision harder

Planning ahead allows you to choose whether to:

- Keep working

- Retire fully

- Or transition gradually

Check Your Exact Retirement Age (State Pension Age Calculator)

Your exact retirement age depends on your date of birth, not just general rules like 66 or 67.

The most accurate way to confirm this is by using the official GOV.UK State Pension age calculator.

What the Calculator Shows

When you use the tool, it tells you:

- The exact date you will reach State Pension age

- When you can claim your State Pension

- Your Pension Credit qualifying age

- When you may become eligible for certain benefits (like free bus travel)

Why You Should Use It

Even small differences in your birth date can change your retirement age.

For example:

- Someone born a few months earlier may retire at 66

- Someone born later may retire at 67

This is due to the phased increase currently in progress.

What Is the Retirement Age UK Calculator?

When people search for:

- “what is the retirement age UK calculator”

- “state pension age calculator”

They are referring to this official GOV.UK tool.

It is the only reliable way to get your exact pension age.

Important Reminder

- General guides (like this article) explain the system

- The calculator gives your personal answer

Always check your own date to avoid planning mistakes.

READ: Equality Act Protected Characteristics: 2026 Importance for Care Work

What This Means for Care Workers & Providers

For many people, retirement planning is straightforward. For care workers and care providers, it is not.

The Reality of Working in Care

Care work is:

- Physically demanding

- Emotionally intensive

- Often underpaid

Yet the UK state pension age is increasing, which means many carers must:

- Work longer than previous generations

- Delay retirement plans

- Rely more on personal savings

This creates a real gap between what people can do physically and what the system expects.

The Hidden Risk Most Care Workers Miss

Many carers assume: “I’ll retire when I reach State Pension age.”

But in practice:

- Burnout often happens earlier

- Health issues may limit working ability

- Income may not be enough to stop working

This is where problems start.

What Care Providers Should Pay Attention To

If you run or manage a care business:

- Your workforce is ageing

- Staff may struggle to work into their late 60s

- Retention becomes harder as pension age increases

This directly impacts:

- Staffing stability

- Recruitment costs

- Service delivery quality

What You Should Start Doing Now

Whether you are a carer or a provider:

- Understand your exact retirement age early

- Build additional income sources beyond the State Pension

- Consider workplace pension contributions seriously

- Plan for a gradual transition, not a sudden stop

Expert Insight (What We See in Practice)

In real-world care settings, Many carers underestimate how rising pension age affects their long-term income and ability to retire comfortably.

They often:

- Start planning too late

- Rely too heavily on the State Pension

- Ignore the gap between early retirement and pension access

Conclusion

Retirement in the UK is no longer a fixed milestone; it is a moving target shaped by policy, economics, and life expectancy. The shift from 66 to 67, and eventually to 68, reflects a system under pressure to stay sustainable. But for individuals, especially those working in care, this creates a new reality:

You can no longer rely on the State Pension alone or assume retirement will happen at a predictable age.

For care workers, the challenge runs deeper. The job demands physical strength, emotional resilience, and long-term commitment, yet the system expects many to continue working well into their late 60s. Without proper planning, this gap between expectation and reality can lead to financial stress and delayed retirement.

The key is simple: Understand your timeline early, plan your income deliberately, and take control of your retirement decisions before the system forces them on you.

Need Expert Support Navigating Retirement, Pensions, and Care-Related Financial Planning?

Care Sync Experts supports care providers, families, and healthcare organisations across the UK with clear, practical guidance on State Pension age changes, retirement planning, and the wider funding systems that impact long-term financial stability.

From helping individuals understand when they can retire, how much State Pension they may receive, and how pension age increases affect their future, to guiding care organisations through workforce planning, compliance expectations, and financial sustainability strategies, our specialists simplify complex government policies into clear, actionable steps.

Whether you need help understanding UK State Pension age changes, private pension access rules, or how retirement planning affects care workforce stability, our team delivers structured guidance aligned with current UK health and social care standards.

Plan ahead with confidence while ensuring your organisation stays informed, compliant, and prepared for the future.

Contact Care Sync Experts today to receive expert guidance on retirement planning, pension changes, and care-related financial strategy with clarity and confidence.

FAQ

Can I retire at 60 and get State Pension?

No, you cannot claim the State Pension at 60 in the UK.

The State Pension is only available once you reach the official pension age (currently 66–67, depending on your birth date).

You can retire at 60, but you must rely on:

Personal savings

Workplace or private pensions (if accessible)

This creates a gap of several years without State Pension income, which you must plan for.

What age can I legally retire in the UK?

There is no legal retirement age in the UK.

You can:

Retire whenever you choose

Continue working beyond State Pension age

Employers cannot force you to retire unless there is a valid occupational reason (e.g. certain physically demanding roles with legal limits).

How many years do I have to work in the UK to get a pension?

You need at least:

10 years of National Insurance contributions to qualify for any State Pension

35 years to receive the full amount

If you have fewer than 35 years:

You will receive a reduced pension

You can also top up missing years through voluntary contributions.

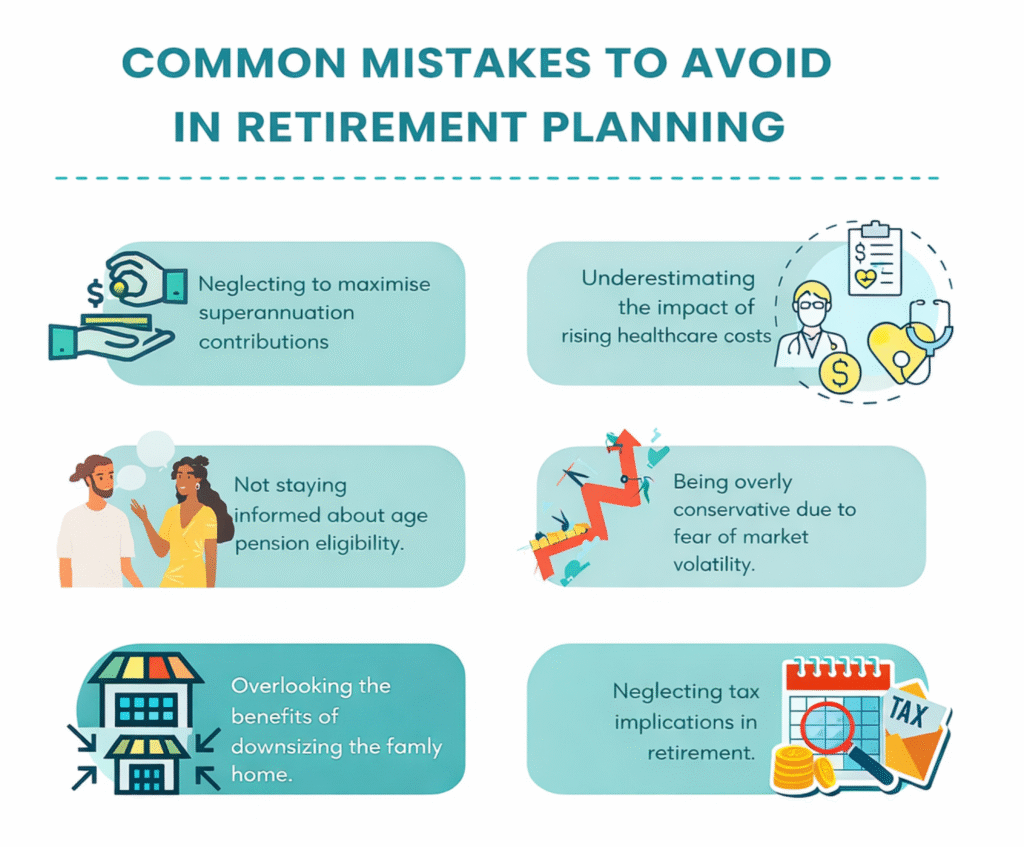

What are the biggest mistakes to avoid when retiring?

Many people make avoidable mistakes that affect their retirement income.

The most common ones include:

Relying only on the State Pension

Starting retirement planning too late

Underestimating how long retirement will last

Ignoring gaps between early retirement and pension access

Not checking their exact pension age.

For care workers, especially, the biggest mistake is assuming, “I’ll just retire when I reach pension age”.

In reality, health, job demands, and income levels often make this harder than expected.

Would you like to receive update from CareSync Experts?

All rights reserved. Copyright © - Care Sync Experts.